Reopening your Business amidst COVID-19: GABB June 9

Russ Hall, Action Coach.

Reopening a business after a shutdown will be a spring, and could take more effort and preparation than shutting it down.

That’s what business coach Russ Hall said to the Georgia Association of Business Brokers during the group’s weekly videoconference on June 9.

Watch a video of his presentation at this link.

View Russ’s PPT presentation here. Rethink Reinvent Reopen PPT

Hall is a GABB affiliate and an Action Coach with an organization focused on helping the owners and teams of small businesses improve performance so that they can improve their lives. Business brokers and others who may be solopreneurs can use these suggestions to garner positive PR and visibility in the community, Hall said.

Hall’s presentation gave business professionals something they can use to stay engaged with people that’s positive and forward-thinking as opposed to negative and a downer.

A former US Naval Aviator, Hall spent 21 years with a Fortune 100 company in the Healthcare Technology sector, leading and managing teams in Sales and Customer Service. He earned a Master’s in Industrial-Organizational Psychology at the University of Georgia, studying the application of evidence-based methods to the improvement of individuals and teams in business and other organizations.

The GABB is the state’s largest and most prominent association of professionals dedicated to the purchase and sale of businesses and franchises, and operates the state’s only professional real estate school dedicated to business brokering.

To join the GABB’s Tuesday meetings, please go to

https://us02web.zoom.us/j/95506520094?pwd=WXdtNjhQVmRSWWdDNk5nV2lHZnNKdz09

Meeting ID: 955 0652 0094

Password: 054703

One tap mobile

+13017158592,,95506520094#,,1#,054703# US (Germantown)

+13126266799,,95506520094#,,1#,054703# US (Chicago)

Dial by your location

+1 301 715 8592 US (Germantown)

+1 312 626 6799 US (Chicago)

+1 929 205 6099 US (New York)

+1 253 215 8782 US (Tacoma)

+1 346 248 7799 US (Houston)

+1 669 900 6833 US (San Jose)

Meeting ID: 955 0652 0094

Password: 054703

Find your local number: https://us02web.zoom.us/u/kdNI1qfTxN

Borrowing from Retirement Savings under CARES Act

John Mills

Concerned about your financial future due to the COVID-19 Crisis? John Mills of Tax Centers of Georgia told members of the GABB about ways you can borrow from your retirement savings without penalty and other tax strategies.

As the COVID-19 virus wreaks havoc on our personal life and financial markets, Mills discussed little known strategies to help businesses and individuals negotiate current financial hardships. The Georgia Association of Business Brokers (GABB) is hosting weekly meetings to answer members’ questions during this pandemic.

A recording of the presentation is linked here.

Mr. Mills, a partner in Tax Centers of Georgia, said that the CARES Act provides an unusual opportunity to get access to your 401k or IRA investments without age restrictions or penalties.

He said many tax experts think “average” income earners could be paying as much as 37-54% in taxes in the near future. He discussed how and investor could add hundreds of thousands dollars of tax-free cash flow to retirement income without any additional savings.

Under the CARES Act, who can get money out of a 401k and/or IRA? Anyone:

- Who is diagnosed with COVID-19 by a test approved by the Centers for Disease Control and Prevention.

- Whose spouse is dependent (generally a qualifying child or relative who receives more than half of his or her support from you) is diagnosed with COVID-19 by such a test.

- Who experiences adverse financial consequences as a result of quarantine, furlough, layoff, or having work hours reduced due to COVID-19.

- Who is unable to work because of lack of child care due to COVID-19 and experiences adverse financial consequences as a result.

- Who owns or operates a business that has closed or had operating hours reduced due to COVID-19 and has experienced adverse financial consequences as a result.

- Who has experienced adverse financial consequences due to other COVID-19 related factors to be specified in future IRS guidance.

COVID-19 401k/IRA Plan Details

- Loans will move from 50% or $50,000 to 100% or $100,000 that you can borrow. This options ends on September 23rd. Your plans loan rates can vary from other plans. You then pay back the loan over 5 years (this can be done with payroll deduction and dramatically increase your savings above the IRS rules).

- If you qualify (based on COVID-19 rules) you can withdraw up to $100,000. You will not be subject to the IRS under 59 ½ rule requiring a 10% penalty. End date for this is 12/31.

- If taken as a distribution, taxes owed can be spread over three years or you can choose to pay the taxes lump sum at the end of three years and skip the tax now.

- This is a one-time opportunity, Mills said.

Option #1: Loan

- Take up to a $100,000 loan from your 401k plan or any other lesser amount.

- Pay back the loan through payroll deduction over 5 years or, in a lump sum at the end of five years. Be your own bank! If you can afford more than the $20,000 limit of your normal contribution, you can now deposit $40,000 per year into your 401(k) (normal contribution plus loan each year.

- Your interest rate may be PRIME (currently about 3.25%). Each plan can vary on the rate, but rates are at an all time low.

- You now have $100,000 in your hands, income tax free.

- Just because you could take a loan, doesn’t mean you should, Mills advised.

Option #2: Distribution

- Take” the full $100,000 as a distribution from your 401k or IRA

- This could be the only time in your lifetime that you can get money out of your pre-tax account while under 59 ½ without a 10% penalty.

- The tax can be spread over three years (Due April 2021, 2022 and 2023)

- Assuming a 24% tax rate, that would mean only $8,000 in tax each year. This can be paid from savings or any other non-qualified investment you may have. If pay in 4 installments (1 immediate and 3 more over 2021-23) it would mean 4 installments of only $6,000.

- How does that benefit you to pay these small taxes over 3 years?

Alternative #1: Roth Conversions

- There is no limit on the amount you can convert from IRA or 401K to Roth

- The CARES ACT however limits the amount you can draw out of your IRA or 401k without the 10% penalty ($100,000 “per person”)

- The Roth will still have the 10% penalty before age 59 ½ and even if over that age you must hold the Roth for 5 years before accessing any of the money.

- Depending on where you invest the Roth money (Stocks, Bonds, Mutual Fds etc.) you still carry all the risk as you did in the 401(k).

What else can you do with the money?

- What if we could get the money to grow tax-deferred (the $100,000) and have it come out 100% Tax-FREE (like the Roth)?

- What if you passed away prematurely and your family then received a large sum, potentially 3 times the amount of money you took out, again…100% Tax-FREE?

- What if you had a chronic illness or required a Long-Term Care stay and you could have money to help cover your stay…100% TAX-FREE?

- What if you had a short-term financial need and you could access this same money again without any 10% governmental penalty or tax BEFORE age 59 ½ ?

Can I really do that?… YES

- Borrow OR take your distribution (or any part of the maximum) and place it in a 7702 plan using life insurance vehicles. Immediate potential benefit for your family should you pass of $336,000*

- Cash then grows tax-deferred and comes out tax free for your retirement or whenever you might need it **.

- Take your tax-free income for 10, 20 years or possibly longer in retirement.

- Receive proceeds in case of a chronic illness or Long-term care need…TAX-FREE.

- Cover a college education or wedding…TAX-FREE.

To find out more, Mills invites businesses and individuals to contact him.

Linked below is Mr. Mills’ PowerPoint presentation.

Cares Act Pwpt- .John Mills (1)-1

Read More

Pandemic Will Impact Business Valuations

The COVID-19 pandemic is going to affect the valuation of businesses, and professionals are likely to take into account a wider number of factors when determining the fair market value of a business.

That’s what two business valuation experts told the Georgia Association of Business Brokers in a conference call on Tuesday, May 26. Dan Browning is the founder and President of DB Consulting, Inc. and David H. Hern, CPA/ABV, ASA, CEPA, a financial analyst with Sofer Advisors spoke to the GABB online. View the conference online here.

“The biggest issue is uncertainty, which heightens the risk, and higher risk leads to lower value,” Browning said. People who assign values to businesses are, by their nature, trying to predict future business conditions, which is tricky anytime, but particularly now. While many businesses have suffered, some businesses “have gone gangbusters,” Browning said. The cost of capital has actually gone down for some businesses, specifically those that have been able to obtain SBA-backed assistance in the form of grants or low-interest loans.

However, some valuation clients are “taking advantage of uncertainty,” Hern said. Some clients are using this time to “do tricky estate planning, issue equity grants, possibly get values frozen below normal,” he said.

If a business valuation was triggered before the onset of the pandemic in the US, some will argue it’s a subsequent event, and should not affect the pre-crisis value. Browning said he has started including an appendix, a disclaimer, calling COVID-19 a subsequent event, which didn’t affect value as of the valuation date.

Browning shared a timeline from respected business valuation expert Jim Hitchner who tracks the impact of the virus on various markets.

Hern shared a Sofer analysis of the mobility of the U.S. Market Mobility of US Market Sofer document

Restaurants have been seriously impacted by the crisis, and many are trying to decide whether it’s worth reopening. Some, like pizza restaurants, have adapted better to a takeout model.

Restaurant broker Dominique Maddox said many of his clients are opting not to reopen and are trying to sell their assets and get out from a multi-year lease. Pizza concepts were able to keep going strong, Maddox said.

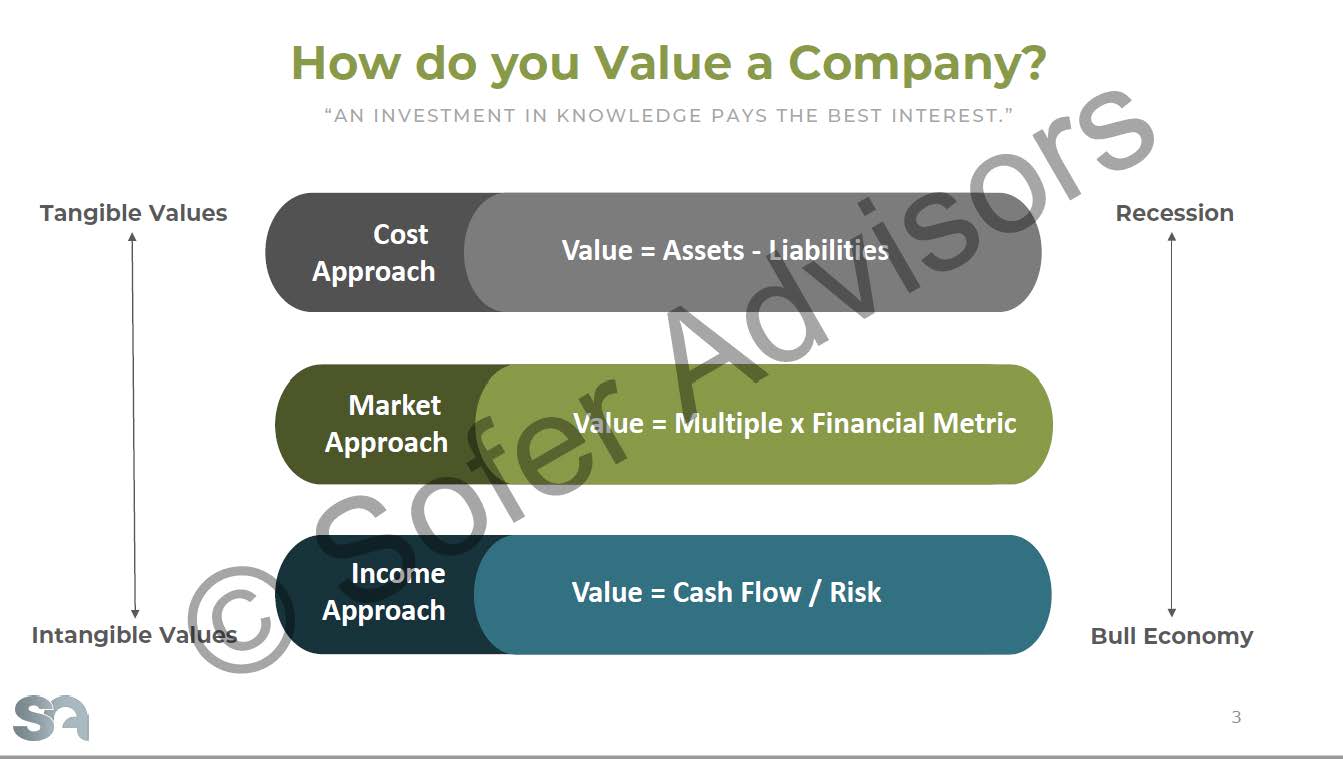

Hern cited three approaches to business valuation: Cost Approach, in which the value of the business is equal to their assets minus liabilities. The Market Approach determines the value of a business based on a multiple and a financial metric. The Income Approach sets the value at cash flow divided by risk.

Hern cited three approaches to business valuation: Cost Approach, in which the value of the business is equal to their assets minus liabilities. The Market Approach determines the value of a business based on a multiple and a financial metric. The Income Approach sets the value at cash flow divided by risk.

The methods skew towards tangible values during a recession, and during bull economy tends to more intangible values. Hern says he’s been running a variety of scenarios taking into account whether the economic recovery may be V-shaped, U-shaped or something else. Browning predicted a W-shaped recovery, with ups and downs.

Businesses may be getting valuations that specify a range of values instead of a single value, Browning said.

“It’s important not to get too negative,” Browning said. “There is a going to be a recovery, there is going to be coming out of all of this.” The recovery may be bumpy, but it will come.

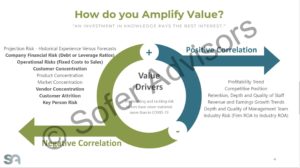

Hern is recommending that business owners prepare their businesses to be in the best shape for the future, fixing problems. You can amplify value by reducing the customer concentration, reducing debt, improving their competitive position, improving staff depth and retention, etc.

“Companies that have fixed these types of issues will sell for better value,” Hern said.

Hern said he will be looking at vendor concentration in the future when valuing a business.

“Doing business is going to be more expensive going forward,” said Browning. Businesses are going to have to buy extra cleaning supplies, extra protective gear, more training of employees.

Hern’s presentation: GABB Sofer

Dan Browning is the founder and President of DB Consulting, Inc. His credentials include:

Dan Browning is the founder and President of DB Consulting, Inc. His credentials include:

- Master Analyst in Financial Forensics (MAFF) from the National Association of Certified Valuators and Analysts, originally awarded August 1999

- Accredited in Business Appraisal Review (ABAR) from the National Association of Certified Valuators and Analysts, originally awarded March 2010

- Georgia Association of Business Brokers (Affiliate Member)

- State Bar of Georgia (Active Member; Eminent Domain and Nonprofit Law Section Memberships)

- Editorial Board, Business Appraisal Practice (IBA Journal) 2013-2015

- University of Notre Dame, Master of Arts (Government), January 1995

- Emory University School of Law, Juris Doctor, May 1992

- Emory University, Bachelor of Arts, May 1985; Phi Beta Kappa

David H. Hern, CPA/ABV, ASA, CEPA, is a highly qualified financial analyst with Sofer Advisors.He has exceptional credentials in determining the true, comprehensive value of an organization. In addition, he has something even more rare: a proven ability to simply and clearly communicate analysis to boards of directors, legal and financial advisors, Company management (CEOs, CFOs, controllers, etc.) and private equity portfolio managers. Mr. Hern offers litigation assistance, estate and tax planning, and business enterprise valuations for various privately-held and public companies. He has been recognized for enabling organizations to determine their enterprise and equity value for a variety of situations

David H. Hern, CPA/ABV, ASA, CEPA, is a highly qualified financial analyst with Sofer Advisors.He has exceptional credentials in determining the true, comprehensive value of an organization. In addition, he has something even more rare: a proven ability to simply and clearly communicate analysis to boards of directors, legal and financial advisors, Company management (CEOs, CFOs, controllers, etc.) and private equity portfolio managers. Mr. Hern offers litigation assistance, estate and tax planning, and business enterprise valuations for various privately-held and public companies. He has been recognized for enabling organizations to determine their enterprise and equity value for a variety of situations

Education

- Georgia Institute of Technology, Scheller College of Business, Atlanta GA. Masters of Business Administration, Finance emphasis.

- Georgia Institute of Technology, Scheller College of Business, Atlanta, GA. Bachelors of Science, Management with Accounting emphasis.

Certifications

- Certified Public Accountant (CPA) — State of Georgia

- Accredited in Business Valuation (ABV)

- Accredited Senior Appraiser (ASA)

- Certified Exit Planning Advisor (CEPA)

Read More

CDC Guidelines for Opening Restaurants, BarsChildcare Centers, other

The Atlanta-based Centers for Disease Control has released a document with the agency’s initiatives, activities, and tools in support of the Whole-of- Government response to COVID-19.

The document outlines recommended procedures for restaurants and bars, healthcare facilities, schools, childcare centers and others. Here’s an excerpt:

INTERIM GUIDANCE FOR RESTAURANTS AND BARS

This guidance provides considerations for businesses in the food-service industry (e.g., restaurants and bars) on ways to maintain healthy business operations and a safe and healthy work environment for employees, while reducing the risk of COVID-19 spread for both employees and customers. Employers should follow applicable Occupational Safety and Health Administration (OSHA) and CDC guidance for businesses to plan and respond to COVID-19. All decisions about implementing these recommendations should be made in collaboration with local health officials and other State and local authorities who can help assess the current level of mitigation needed based on levels of COVID-19 community transmission and the capacities of the local public health and healthcare systems. CDC is releasing this interim guidance, laid out in a series of three steps, to inform a gradual scale up of activities towards pre-COVID-19 operating practices. The scope and nature of community mitigation suggested decreases from Step 1 to Step 3. Some amount of community mitigation is necessary across all steps until a vaccine or therapeutic drug becomes widely available.

Scaling Up Operations

In all Steps:

- Establish and maintain communication with local and State authorities to determine current mitigation levels in your community.

- Consider assigning workers at high risk for severe illness duties that minimize their contact with customers and other employees (e.g., man-aging inventory rather than working as a cashier, managing administrative needs through telework).

- Provide employees from higher transmission areas (earlier Step areas) telework and other options as feasible to eliminate travel to workplaces in lower transmission (later Step) areas and vice versa.

- Step 1: Bars remain closed and restaurant service should remain limited to drive-through, curbside take out, or delivery with strict social distancing.

- Step 2: Bars may open with limited capacity; restaurants may open dining rooms with limited seating capacity that allows for social distancing.

- Step 3: Bars may open with increased standing room occupancy that allows for social distancing; restaurants may operate while maintaining social distancing.

Safety Actions

Promote healthy hygiene practices (Steps 1-3)

- Enforce hand washing, covering coughs and sneezes, and use of a cloth face coverings by employees when near other employees and

- Ensure adequate supplies to support healthy hygiene practices for both employees and customers including soap, hand sanitizer with at least 60 percent alcohol (on every table, if supplies allow), paper towels, and tissues.

- Post signs on how to stop the spread of COVID-19 properly wash hands, promote everyday protective measures, and properly wear a face covering.

Intensify cleaning, disinfection, and ventilation (Steps 1-3)

- Clean and disinfect frequently touched surfaces (for example, door handles, work stations, cash registers) at least daily and shared objects (for example, payment terminals, tables, countertops/bars, receipt trays, condiment holders) between use. Use products that meet EPA’s criteria for use against SARS-CoV-2 and that are appropriate for the surface. Prior to wiping the surface, allow the disinfectant to sit for the necessary contact time recommended by the manufacturer. Train staff on proper cleaning procedures to ensure safe and correct application of disinfectants.

- Make available individual disinfectant wipes in bathrooms.

- Wash, rinse, and sanitize food contact surfaces, food preparation surfaces, and beverage equipment after use.

- Avoid using or sharing items such as menus, condiments, and any other food. Instead, use disposable or digital menus, single-serving condiments, and no-touch trash cans and doors.

- Use touchless payment options as much as possible, when available. Ask customers and employees to exchange cash or card payments by placing on a receipt tray or on the counter rather than by hand. Clean and disinfect any pens, counters, or hard surfaces between use or customer.

- Use disposable food service items (utensils, dishes). If disposable items are not feasible, ensure that all non-disposable food service items are handled with gloves and washed with dish soap and hot water or in a dishwasher. Employees should wash their hands after removing their gloves or after directly handling used food service items.

- Use gloves when removing garbage bags or handling and disposing of trash and wash hands afterwards.

- Avoid using food and beverage containers or utensils brought in by customers.

- Ensure that ventilation systems operate properly and increase circulation of outdoor air as much as possible such as by opening windows and doors. Do not open windows and doors if doing so poses a safety risk to employees, children, or customers.

- Take steps to ensure that all water systems and features (for example, drinking fountains, decorative fountains) are safe to use after a prolonged facility shutdown to minimize the risk of Legionnaires’ disease and other diseases associated with water.

Promote social distancing

Step 1

- Limit service to drive-through, delivery, or curb-side pick-up options only.

- Provide physical guides, such as tape on floors or sidewalks to ensure that customers remain at least six feet apart in lines or ask customers to wait in their cars or away from the establishment while waiting to pick up food. Post signs to inform customers of food pickup protocols.

- Consider installing physical barriers, such as sneeze guards and partitions at cash registers, or other food pickup areas where maintaining physical distance of six feet is difficult.

- Restrict the number of employees in shared spaces, including kitchens, break rooms, and offices to maintain at least a six-foot distance between people.

- Rotate or stagger shifts to limit the number of employees in the workplace at the same time.

Step 2

Provide drive-through, delivery, or curb-side pick-up options and prioritize outdoor seating as much as possible.

- Reduce occupancy and limit the size of parties dining in together to sizes that ensure that all customer parties remain at least six feet apart (e.g., all tables and bar stools six feet apart, marking tables/stools that are not for use) in order to protect staff and other guests.

- Provide physical guides, such as tape on floors or sidewalks and signage on walls to ensure that customers remain at least six feet apart in lines or waiting for seatings.

- Ask customers to wait in their cars or away from the establishment while waiting to be seated. If possible, use phone app technology to alert patrons when their table is ready to avoid touching and use of “buzzers.”

- Consider options for dine-in customers to order ahead of time to limit the amount of time spent in the establishment.

- Avoid offering any self-serve food or drink options, such as buffets, salad bars, and drink stations.

- Install physical barriers, such as sneeze guards and partitions at cash registers, bars, host stands, and other areas where maintaining physical distance of six feet is difficult.

- Limit the number of employees in shared spaces, including kitchens, break rooms, and offices to maintain at least a six-foot distance between people.

Step 3

- Provide drive-through, delivery, or curbside pick-up options and prioritize outdoor seating as much as possible.

- Consider reducing occupancy and limiting the size of parties dining in together to sizes that ensure that all customer parties remain at least six feet apart (e.g., all tables and bar stools six feet apart, marking tables/stools that are not for use) in order to protect staff and other guests.

- Provide physical guides, such as tape on floors or sidewalks and signage on walls, to ensure that customers remain at least six feet apart in lines or waiting for seatings.

- If possible, use phone app technology to alert patrons when their table is ready to avoid touching and use of “buzzers.”

- Consider options for dine-in customers to order ahead of time to limit the amount of time spent in the establishment.

- Avoid offering any self-serve food or drink options, such as buffets, salad bars, and drink stations.

- Install physical barriers, such as sneeze guards and partitions at cash registers, bars, host stands, and other areas where maintaining physical distance of six feet is difficult.

Train all staff (Steps 1-3)

- Train all employees in the above safety actions while maintaining social distancing and use of face coverings during training.

Monitoring and Preparing

Checking for signs and symptoms (Steps 1-3)

- Consider conducting daily health checks (e.g., temperature and symptom screening) of employees.

- If implementing health checks, conduct them safely and respectfully, and in accordance with any applicable privacy laws and regulations. Confidentiality should be respected. Employers may use examples of screening methods in CDC’s General Business FAQs as a guide.

- Encourage staff who are sick to stay at home.

Plan for when an employee becomes sick (Steps 1-3)

- Employees with symptoms of COVID-19 (fever, cough, or shortness of breath) at work should immediately be sent to their home.

- Inform those who have had close contact to a person diagnosed with COVID-19 to stay home and self- monitor for symptoms, and to follow CDC guidance if symptoms develop. If a person does not have symptoms follow appropriate CDC guidance for home isolation.

- Establish procedures for safely transporting anyone sick to their home or to a healthcare facility.

- Notify local health officials, staff, and customers (if possible) immediately of any possible case of COVID-19 while maintaining confidentiality consistent with the Americans with Disabilities Act (ADA) and other applicable federal and state privacy laws.

- Close off areas used by a sick person and do not sure them until after cleaning and disinfection. Wait 24 hours before cleaning and disinfecting. If it is not possible to wait 24 hours, wait as long as possible. Ensure safe and correct application of disinfectants and keep disinfectant products away from children.

- Advise sick staff members not to return until they have met CDC’s criteria to discontinue home isolation.

Maintain healthy operations (Steps 1-3)

- Implement flexible sick leave and other flexible policies and practices, such as telework, if

- Monitor absenteeism of employees and create a roster of trained back-up

- Designate a staff person to be responsible for responding to COVID-19 concerns. Employees should know who this person is and how to contact them.

- Create and test communication systems for employees for self-reporting and notification of exposures and closures.

- Support coping and resilience among employees.

Closing

Steps 1-3

- Check State and local health department notices about transmission in the area daily and adjust operations accordingly.

- Be prepared to consider closing for a few days if there is a case of COVID-19 in the establishment and for longer if cases increase in the local area.

SBA Safe Harbor Ruling Welcomed by Borrowers

Businesses that borrowed less than $2 million under the Paycheck Protection Program will get an automatic safe harbor, according to a Small Business Administration announcement issued May 13.

“Any borrower that, together with its affiliates, received PPP loans with an original principal amount of less than $2 million will be deemed to have made the required certification concerning the necessity of the loan request in good faith,” according to the SBA’s responses to FAQ’s about PPP loans.

The SBA had previously said it would review any PPP loans exceeding $2 million, according to the ABA Banking Journal.

As of May 13, the SBA said it had approved 2,686,493 loans totaling $192,565,254,187 in the second round of the PPP. The average loan size in the second round was $71,679, issued by 5,428 lenders. In round one, 1,661,367 loans totalling $342,277,999,103 from 4,975 lenders were approved, the SBA said.

Borrowers that received PPP loans for amounts over $2 million will be subject to review by the SBA for compliance with program requirements, including the certification of economic need. “If SBA determines in the course of its review that a borrower lacked an adequate basis for the required certification concerning the necessity of the loan request, SBA will seek repayment of the outstanding PPP loan balance and will inform the lender that the borrower is not eligible for loan forgiveness,” SBA said.

Borrowers who repay their loans after receiving notification from the SBA will not be subject to administrative enforcement or referrals to other agencies, the SBA said. Additionally, SBA’s determination regarding the necessity of the loan request will not affect the SBA loan guarantee.

SBA will also automatically extend until May 18 the safe harbor deadline to allow PPP borrowers “an opportunity to review and consider” the new guidelines. Borrowers do not need to apply for this extension. This extension will be promptly implemented through a revision to the SBA’s interim final rule providing the safe harbor.

SBA said this safe harbor is appropriate because borrowers with loans below $2 million “are generally less likely to have had access to adequate sources of liquidity in the current economic environment than borrowers that obtained larger loans.” The SBA also said “this safe harbor will also promote economic certainty as PPP borrowers with more limited resources endeavor to retain and rehire employees. In addition, given the large volume of PPP loans, this approach will enable SBA to conserve its finite audit resources and focus its reviews on larger loans, where the compliance effort may yield higher returns.”

“Importantly, borrowers with loans greater than $2 million that do not satisfy this safe harbor may still have an adequate basis for making the required good-faith certification, based on their individual circumstances in light of the language of the certification and SBA guidance. SBA has previously stated that all PPP loans in excess of $2 million, and other PPP loans as appropriate, will be subject to review by SBA for compliance with program requirements set forth in the PPP Interim Final Rules and in the Borrower Application Form. If SBA determines in the course of its review that a borrower lacked an adequate basis for the required certification concerning the necessity of the loan request, SBA will seek repayment of the outstanding PPP loan balance and will inform the lender that the borrower is not eligible for loan forgiveness. If the borrower repays the loan after receiving notification from SBA, SBA will not pursue administrative enforcement or referrals to other agencies based on its determination with respect to the certification concerning necessity of the loan request. SBA’s determination concerning the certification regarding the necessity of the loan request will not affect SBA’s loan guarantee.”

The SBA’s list of FAQ’s related to the PPP is frequently updated.

Read More