Getting Back to Business After the COVID-19 Pandemic

Despite our various technological advances and the complexity of our society, disease can instantly change the course of history. Not having a robust global system for dealing with disease and pandemics comes with a hefty price tag. In the case of the COVID-19 economic crisis, the price tag will no doubt be in the trillions.

You can’t control what has happened, but you can focus on what to do when the pandemic is over and life begins to slowly return to normal. In his article “How to Hit the Ground Running After the Pandemic,” Inc. contributing editor Geoffrey James explores what businesses need to do to jumpstart their operations once the pandemic is history.

Understand that this pandemic will end, and business owners need to be ready to charge back in when the economy rebounds. If history is any indicator, the economy will eventually rebound, James says.

James correctly asserts that businesses need to put together a plan for how they will get up and running as soon as the pandemic is over. His recommendation is to divide your plan and thinking into four distinct categories: Facilities, Personnel, Manufacturing, and Marketing.

Each of these categories has three key questions that business owners should be asking themselves so that their businesses are ready to hit the ground running when COVID-19 is over. Below are a few of the key questions James recommends asking.

- How can we create the most sanitary and disease-free workplace possible?

- Which employees will continue to work from home?

- When there’s a spike in demand, how will we ramp-up?

- What will be our “We’re Back!” marketing message?

The pandemic caught everyone except the experts off guard. Therefore business leaders, think tanks, and politicians alike need to work to develop and implement robust plans to minimize the damage caused by pandemics. Humans and businesses have been “lucky” several times in recent years as we dodged bullets ranging from Ebola to SARS.

As James points out: “Failing to plan is planning to fail.” Businesses need to plan for the recovery, and they need to plan for another pandemic because another economic disaster is possible especially if better planning and decision making are not put in place.

Almost everything about this economic downturn is unique. Take, for example, the fact that the U.S. has just seen its largest-ever economic expansion. The gears and wheels of the economy were spinning along quite quickly before the pandemic hit. This could help restart the economy faster than in past severe economic downturns. In short, many experts feel that this particular economic downturn could be short, but of course, this is speculation. There is no way to know for sure until COVID-19 is in the rearview mirror.

Copyright: Business Brokerage Press, Inc.

The post Getting Back to Business After the COVID-19 Pandemic appeared first on Deal Studio – Automate, accelerate and elevate your deal making.

COVID-19 Advice for Hospitality Businesses

Clearly, some industries are taking a bigger hit from COVID-19 than others. Any industry that requires a great deal of interaction with the public, or where people gather in large groups, are obviously having very tough times. Movie theaters and restaurants, for example, have essentially gone dark. Some restaurants are easing the bloodletting a bit by providing delivery, but in the vast majority of cases, revenue pales in comparison to what it was prior to the pandemic.

While there is no doubt that the hospitality industry is suffering right now, business owners should understand that there are concrete steps they can take now to improve their odds of surviving the pandemic. In this article, we’ll explore a few of these key ideas.

One of the areas every decision maker and business owner in the hospitality industry should be thinking about right now is staff. During a recent industry roundtable discussion, John Howe, chairman of the International Association of Business Intermediaries, pointed out that staffing problems will continue long after the pandemic has paused or is over. He believes that hospitality businesses will have a tough time getting the staff they need, especially in the short run.

His key piece of advice is to work to have a line on people for key positions. This will allow you to at least get back up and running with basic operations. While it may be a while before hospitality businesses are at “full steam,” it is critical that they are able to open up in some fashion, as this will translate into much needed revenue. Hospitality businesses looking to survive the pandemic should focus on making certain that key positions have been filled. In this way, the post-pandemic relaunch can be as smooth as possible.

Founder and President of Cornerstone Business Services, Scott Bushkie, explained that there are a lot of hospitality industry people out of work right now, and this represents a real opportunity. Now, is the perfect time to potentially upgrade staff. There are plenty of experienced and proven hospitality people looking for positions. The new people you bring may come with extra benefits such as bringing their customers, suppliers, and other relationships with them. For those in the hospitality industry who may have always wanted to upgrade their team, now is perhaps the best time in history to do so.

Employees are a foundational element of your business. Improving your staff means you’ve improved your business and boosted your odds of survival. Bringing in new team members can help you prepare for the post-pandemic business environment. It also offers up the potential for you to upgrade an important element within your business.

Copyright: Business Brokerage Press, Inc.

The post COVID-19 Advice for Hospitality Businesses appeared first on Deal Studio – Automate, accelerate and elevate your deal making.

Pandemic Will Impact Business Valuations

The COVID-19 pandemic is going to affect the valuation of businesses, and professionals are likely to take into account a wider number of factors when determining the fair market value of a business.

That’s what two business valuation experts told the Georgia Association of Business Brokers in a conference call on Tuesday, May 26. Dan Browning is the founder and President of DB Consulting, Inc. and David H. Hern, CPA/ABV, ASA, CEPA, a financial analyst with Sofer Advisors spoke to the GABB online. View the conference online here.

“The biggest issue is uncertainty, which heightens the risk, and higher risk leads to lower value,” Browning said. People who assign values to businesses are, by their nature, trying to predict future business conditions, which is tricky anytime, but particularly now. While many businesses have suffered, some businesses “have gone gangbusters,” Browning said. The cost of capital has actually gone down for some businesses, specifically those that have been able to obtain SBA-backed assistance in the form of grants or low-interest loans.

However, some valuation clients are “taking advantage of uncertainty,” Hern said. Some clients are using this time to “do tricky estate planning, issue equity grants, possibly get values frozen below normal,” he said.

If a business valuation was triggered before the onset of the pandemic in the US, some will argue it’s a subsequent event, and should not affect the pre-crisis value. Browning said he has started including an appendix, a disclaimer, calling COVID-19 a subsequent event, which didn’t affect value as of the valuation date.

Browning shared a timeline from respected business valuation expert Jim Hitchner who tracks the impact of the virus on various markets.

Hern shared a Sofer analysis of the mobility of the U.S. Market Mobility of US Market Sofer document

Restaurants have been seriously impacted by the crisis, and many are trying to decide whether it’s worth reopening. Some, like pizza restaurants, have adapted better to a takeout model.

Restaurant broker Dominique Maddox said many of his clients are opting not to reopen and are trying to sell their assets and get out from a multi-year lease. Pizza concepts were able to keep going strong, Maddox said.

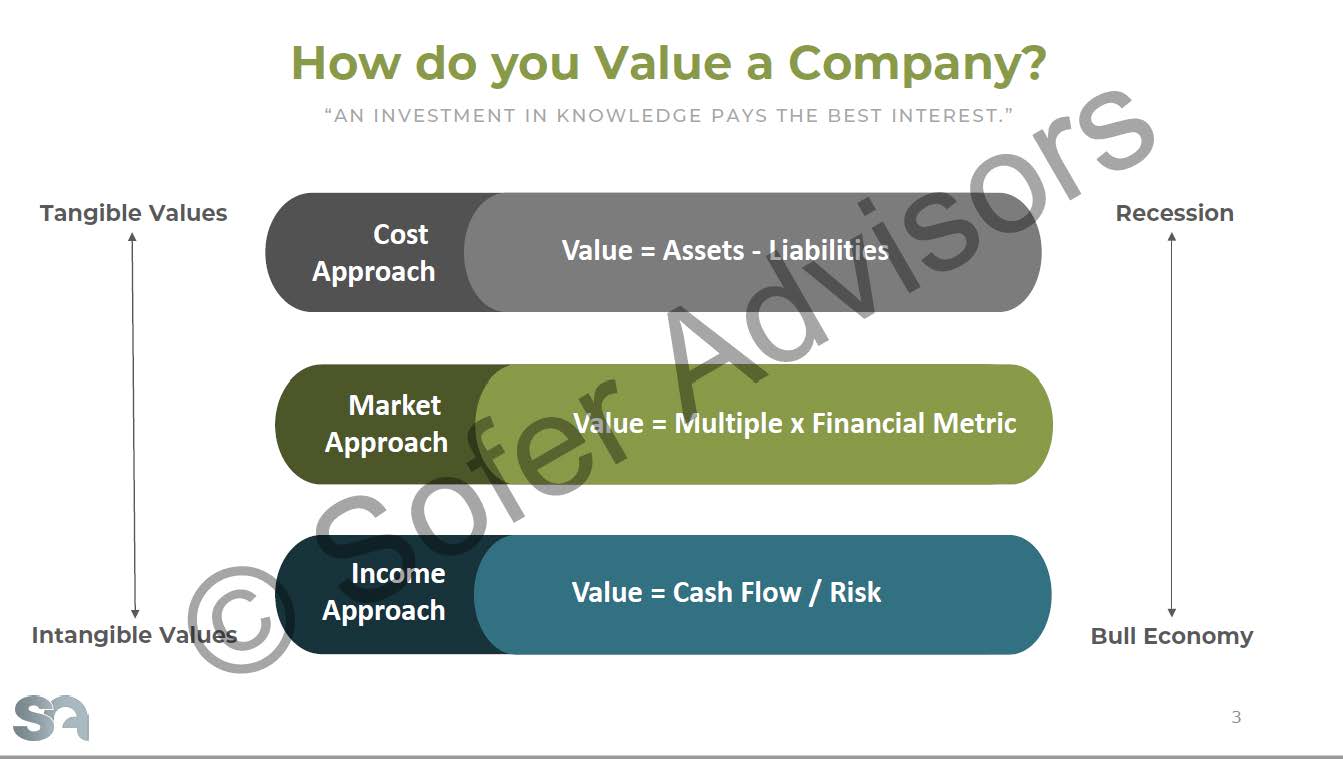

Hern cited three approaches to business valuation: Cost Approach, in which the value of the business is equal to their assets minus liabilities. The Market Approach determines the value of a business based on a multiple and a financial metric. The Income Approach sets the value at cash flow divided by risk.

Hern cited three approaches to business valuation: Cost Approach, in which the value of the business is equal to their assets minus liabilities. The Market Approach determines the value of a business based on a multiple and a financial metric. The Income Approach sets the value at cash flow divided by risk.

The methods skew towards tangible values during a recession, and during bull economy tends to more intangible values. Hern says he’s been running a variety of scenarios taking into account whether the economic recovery may be V-shaped, U-shaped or something else. Browning predicted a W-shaped recovery, with ups and downs.

Businesses may be getting valuations that specify a range of values instead of a single value, Browning said.

“It’s important not to get too negative,” Browning said. “There is a going to be a recovery, there is going to be coming out of all of this.” The recovery may be bumpy, but it will come.

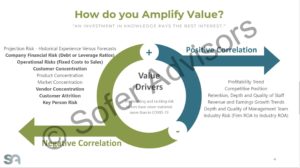

Hern is recommending that business owners prepare their businesses to be in the best shape for the future, fixing problems. You can amplify value by reducing the customer concentration, reducing debt, improving their competitive position, improving staff depth and retention, etc.

“Companies that have fixed these types of issues will sell for better value,” Hern said.

Hern said he will be looking at vendor concentration in the future when valuing a business.

“Doing business is going to be more expensive going forward,” said Browning. Businesses are going to have to buy extra cleaning supplies, extra protective gear, more training of employees.

Hern’s presentation: GABB Sofer

Dan Browning is the founder and President of DB Consulting, Inc. His credentials include:

Dan Browning is the founder and President of DB Consulting, Inc. His credentials include:

- Master Analyst in Financial Forensics (MAFF) from the National Association of Certified Valuators and Analysts, originally awarded August 1999

- Accredited in Business Appraisal Review (ABAR) from the National Association of Certified Valuators and Analysts, originally awarded March 2010

- Georgia Association of Business Brokers (Affiliate Member)

- State Bar of Georgia (Active Member; Eminent Domain and Nonprofit Law Section Memberships)

- Editorial Board, Business Appraisal Practice (IBA Journal) 2013-2015

- University of Notre Dame, Master of Arts (Government), January 1995

- Emory University School of Law, Juris Doctor, May 1992

- Emory University, Bachelor of Arts, May 1985; Phi Beta Kappa

David H. Hern, CPA/ABV, ASA, CEPA, is a highly qualified financial analyst with Sofer Advisors.He has exceptional credentials in determining the true, comprehensive value of an organization. In addition, he has something even more rare: a proven ability to simply and clearly communicate analysis to boards of directors, legal and financial advisors, Company management (CEOs, CFOs, controllers, etc.) and private equity portfolio managers. Mr. Hern offers litigation assistance, estate and tax planning, and business enterprise valuations for various privately-held and public companies. He has been recognized for enabling organizations to determine their enterprise and equity value for a variety of situations

David H. Hern, CPA/ABV, ASA, CEPA, is a highly qualified financial analyst with Sofer Advisors.He has exceptional credentials in determining the true, comprehensive value of an organization. In addition, he has something even more rare: a proven ability to simply and clearly communicate analysis to boards of directors, legal and financial advisors, Company management (CEOs, CFOs, controllers, etc.) and private equity portfolio managers. Mr. Hern offers litigation assistance, estate and tax planning, and business enterprise valuations for various privately-held and public companies. He has been recognized for enabling organizations to determine their enterprise and equity value for a variety of situations

Education

- Georgia Institute of Technology, Scheller College of Business, Atlanta GA. Masters of Business Administration, Finance emphasis.

- Georgia Institute of Technology, Scheller College of Business, Atlanta, GA. Bachelors of Science, Management with Accounting emphasis.

Certifications

- Certified Public Accountant (CPA) — State of Georgia

- Accredited in Business Valuation (ABV)

- Accredited Senior Appraiser (ASA)

- Certified Exit Planning Advisor (CEPA)

Read More

Dealing with COVID-19’s Economic Impact: Planning and Communication are Key

There are many things that you should be doing to deal with the COVID-19 pandemic. At the top of the list is to be proactive. Now is the time to be thinking about how best to position your business after the economy has returned to something near normal. Now is not the time for self-pity. In fact, not preparing for the relaunch of the economy will cost you.

In David Finkel’s recent Inc. article entitled, “10 Things Every Small-Business Owner Needs to Do to Deal with the Impact of COVID-19 on Their Business,” Finkel outlines the 10 key steps business owners should take immediately. Finkel is the author of 12 business books and CEO of Maui Mastermind business coaching company.

There is no way of knowing how long the COVID-19 fueled economic downturn will last, and that means time is of the essence. Business owners, regardless of their particular sector, need to prepare as though the economy could relaunch tomorrow.

Finkel’s 10 Things:

- Take steps to protect your staff and customers from getting sick.

- Tell your customers what safety steps you’re taking.

- Educate your staff on how to stay healthy at work and at home.

- Engage in scenarios planning to deal with how markets could change.

- Enlist vendors and suppliers for help. You should ask them to negotiate payment terms.

- Take steps to plan out your cash flow.

- Open a dialogue with your management team.

- Go on the offensive and look for opportunities.

- Get your team together and brainstorm.

- Be sure your key leaders communicate in a united fashion.

There are definitely some commonalities amongst these 10 important steps. You’ll notice that communication and education are at the heart of most of these points.

There is a lot of fear and uncertainty out there. More than almost any time in modern history now is the time to communicate. All business owners should be advised to communicate with their customers, clients, suppliers, staff, and management team in a clear fashion. Effective communication based around a consistent and logical message can help to reduce fear. The fear sections of the brain are driven by our primordial ancestors’ dread of the unknown lurking in the darkness. Part of being a good leader is to reduce those fears whenever possible.

Another common thread is planning, which includes looking for new opportunities. Whenever there is chaos and fear, there are also opportunities. You should be looking for those opportunities, whether it is improving your own business practices or looking for other companies to buy.

Good communication and planning can help you navigate these choppy waters. Planning for the recovery from COVID-19 pandemic could be the difference between staying in business and going out of business.

Copyright: Business Brokerage Press, Inc.

The post Dealing with COVID-19’s Economic Impact: Planning and Communication are Key appeared first on Deal Studio – Automate, accelerate and elevate your deal making.

How to Make Remote Teams Accountable

One of the many, many changes that COVID-19 has ushered in is the extreme uptick in people working remotely. Social distancing has made working from home a necessity for millions.

The technology that is allowing remote working to take place has matured greatly in the last decade. Today, it is possible for team members to work from virtually any location. Of course, as with most technologies, there is a potential downside. Accountability can become a significant challenge with remote workers. Of course, the more remote workers you have at a given time, the greater the potential challenges will be.

Many businesses are struggling with the phenomenon of remote working, as it is something new for them. Under normal circumstances, large numbers of employees working remotely simply wouldn’t happen. Writing for Inc., Elise Keith, Co-Founder and CEO of Lucid Meetings, recommended key steps businesses should take to help ensure that their employees stay on target while working from home.

Don’t demand high productivity

To be effective, Keith says remote work environments must avoid four major mistakes. Employers, especially those unfamiliar with remote work, often demand too much productivity right out of the gate.

Remote teams can be very productive and even outperform their in-office counterparts. Put everything you’re doing on one of three lists: Start, Stop, Continue. “Challenge yourselves to get the Start and Continue lists as short as possible while still ensuring critical business operations.”

Don’t Assume this is Temporary

It’s a mistake to assume the current pandemic situation is temporary. Even if COVID-19 disappears, other crises will occur, and it makes sense to be prepared. Why not “get good at working remotely?” Teams with good remote working skills are more resilient now. You can be sure your competitors are working remotely, too.

Be Open to Technology

Don’t automatically ban the use of non-approved tools. Now is not the time to fret about what software tools people are using. “You can’t have it both ways. Either give your teams the resources they need to be effective or decrease your expectations,” says David Horowitz, the CEO of Retrium, a platform for running online retrospectives.

Keith suggests creating an expedited process for the adoption of new tools. If your team finds a new tool that boosts productivity, you should consider buying it.

“Software costs pale when compared to the costs of lost opportunity,” Keith points out. Set aside restrictive thinking and become more open-minded and flexible. Remember, your top goal and that of your clients is to stay in business until the pandemic has passed.

Stay Flexible

It’s a mistake for managers to dictate hours and response times. Remote work is, by its nature, going to be more flexible. Trying to micromanage every move digitally is simply not a savvy move and will hurt morale.

Instead, Keith thinks businesses should opt for having a daily meeting via phone or videoconference with the team. Consider having a one-on-one meeting with every team member, also.

Adapt and Survive

“Remote work may be new to you, but that doesn’t make it unproven or risky,” Keith says. “Stop trying to control the situation and focus instead on finding the new opportunities created. Remote work is different, so slow down and learn from many of the excellent resources out there.”

Remote work can be highly effective for you, especially when used correctly.

Copyright: Business Brokerage Press, Inc.

The post How to Make Remote Teams Accountable appeared first on Deal Studio – Automate, accelerate and elevate your deal making.