Economic Injury Disaster Loan (EIDL) Grant FAQ’s

The SBA’s Economic Injury Disaster Loan (EIDL) Program provides small businesses (500 employees or less) and nonprofits with low-interest loans of up to $2 million. The loans can provide vital economic support to small businesses to help overcome the temporary loss of revenue they are experiencing due to COVID-19, according to information posted online by New York state. EIDL interest rates are 3.75% for small businesses and 2.75% for not-for-profits.

Due to the COVID-19 impact on small businesses nationwide, an overwhelming number of loan requests are coming into the GABB’s affiliate banks. Our SBA lenders are working hard to return all emails and phone calls as quickly as possible, and are prioritizing working with their existing customers. We encourage you to contact your lending or depository bank about their participation. For the fastest response time please correspond via email or text.

The law provides that applicants can request up to $10,000; however, it seems that the SBA may scale the advance based on the number of employees an applicant has, according to information posted online by U.S. Sen. Brian Schatz of Hawaii. Based on reports, the SBA may provide $1,000 per employee for up to ten employees. However, SBA has not provided public guidance on how it will determine the amount of the advance. Please check back for updates.

UGA’s Small Business Information Center also is providing information on this program, along with helpful comparisons of the various aid programs available.

New York posted the following information about the EIDL grants on the Empire State Development section of the state website.

As part of the COVID-19 relief effort, borrowers can also apply for an Emergency EIDL Grant from the SBA to request an advance on the loan of up to $10,000.

- SBA will determine the amount of grant based on the information provided by the borrower.

- SBA must distribute the Emergency EIDL within three days of the request.

- The advance will be considered an Emergency EIDL grant.

- The borrower will not be required to pay back the Emergency EIDL Grant even if they are subsequently denied for an EIDL loan.

- In advance of disbursing the advance payment, the SBA will require that the borrower file a certification, under penalty of perjury, that they are eligible to apply for an EIDL loan.

- The Emergency EIDL Grants will end on December 30, 2020.

Who is Eligible to Apply?

The following types of businesses are eligible to apply for the EIDL:

- Small businesses;

- Small agricultural cooperatives,

- Small aquaculture businesses;

- Most private non-profit organizations

- Tribal businesses;

- Cooperative;

- ESOPs with fewer than 500 employees;

- Any individual operating as a sole proprietor; and

- An independent contractor during January 31, 2020 to December 31, 2020.

The SBA generally defines a small business as an entity with 500 employees or less. There are, however, specific size standards depending on the type of business. You can look up the standards for your specific business by NAICS code here.

How to apply:

- Apply directly with the Small Business Administration. Applications can be submitted here.

- Deadline to submit your application is December 21, 2020.

- Businesses are encouraged to submit applications as soon as possible.

FAQ’s

Can I apply for EIDL grants and loans as a sole proprietor, ESOPs, non-profits, or a Tribal business?

•Yes, eligibility has been expanded to include:

- Tribal businesses;

- Cooperative;

- ESOPs with fewer than 500 employees;

- Any individual operating as a sole proprietor; and

- An independent contractor during January 31, 2020 to December 31, 2020.

Can I apply for COVID-19 EIDL with a business operating for less than a year?

- Yes.

Do I need to provide a personal guarantee on EIDL loans?

- The SBA waived any personal guarantee on advances and loans below$200,000.

- For loan amounts over $200,000, the SBA may require personal guarantees.

What are the underwriting criteria for EIDL loans?

- The SBA can approve and offer EIDL loans based solely on an applicant’s credit score or use an appropriate alternative method for determining applicant’s ability to repay.

What can I use the advance payment for?

- Advance payment may be used for:

- Providing paid sick leave to employees;

- Maintaining payroll;

- Meeting increased costs to obtain materials;

- Making rent or mortgage payments; or

- Repaying obligations that cannot be met due to revenue losses.

Will advance payment be deducted from PPP loan forgiveness?

- Yes. If the applicant transfers into a loan made under SBA’s Paycheck Protection Program. The advance payment will be considered when determining loan forgiveness.

When does EIDL grant program end?

The Emergency EIDL Grants will end on December 30, 2020.

ECONOMIC INJURY DISASTER LOAN

What types of businesses are eligible to apply?

- Small businesses;

- small agricultural cooperatives,

- small aquaculture businesses;

- most private non-profit organizations

- Tribal businesses;

- Cooperative;

- ESOPs with fewer than 500 employees;

- Any individual operating as a sole proprietor; and

- An independent contractor during January 31, 2020 to December 31, 2020.

What is the definition of a small business under this program?

- Businesses with 500 or fewer employees. The SBA size standards show by NAICS code for each type of business: https://sba.gov/size-standards

How much can I borrow?

- Businesses may qualify for loans up to $2 million.

- Eligibility is based on the size and type of business.

What are the loan interest rates?

- The interest rate is 3.75% for small businesses.

- The interest rate for non-profits is 2.75%.

How can I use loan funds?

- Loan funds can be used as working capital to pay fixed debts, payroll, accounts payable and other bills that could have been paid had the disaster not occurred.

What is fixed debt?

- Fixed debt is a permanent debt, or a debt continuing for an extended period.

How long do I have to submit my loan documents?

- Submit your application as soon as possible. Applications can be submitted at https://disasterloan.sba.gov/ela/Information/ApplyOnline

- Deadline to submit your application is December 21, 2020.

How can I get assistance with my SBA application?

- Governor Kemp announced a partnership between the University of Georgia Small Business Development Center, the Georgia Department of Community Affairs and the Georgia Department of Economic Development to provide the small businesses of Georgia with assistance during this time of need.

- SBDC: https://nysbdc.org/appointment.html

- EAC: https://esd.ny.gov/sites/default/files/EAC%20Contact%20List%20for%20ES D%20Website%20-%20Sheet1.pdf

- CDFI: https://esd.ny.gov/sites/default/files/CDFI21_ContactList.pdf

As a small business, what documents would I need to submit to prove my business suffered economic injury as a result of the Coronavirus?

- Substantial economic injury occurs when a business concern is unable to meet its obligations as they mature or to pay its ordinary and necessary operating expenses.

- Establishing economic injury is a comparison between the financial information from the period in the prior year to the injury period of the current year (this period must be associated to the disaster and cannot be attributed to a downturn in local economy or other unrelated issues).

- The loans are not intended to replace lost sales or profits, rather they are intended to pay fixed debts, payroll, accounts payable, and other expenses that could have been paid had the disaster not occurred.

How can a business owner document physical presence in the declared disaster area?

- An applicant must show that they have tangible presence such as lease, property address, property tax

- Merely having a P.O. Box in the disaster area would not qualify as a physical presence.

What are the repayment terms of the loan?

- SBA offers loans with long-term repayments in order to keep payments affordable, up to a maximum of 30

- Terms are determined on a case-by-case basis, based upon each borrower’s ability to repay.

Will someone notify an application if information is missing from an application?

- A SBA loan officer works with you to provide all the necessary information needed to reach a loan determination.

- The goal is to arrive at a decision on your application within 2-3 weeks.

How will the business owner know if the loan request has been approved?

- A loan officer will contact you to discuss the loan recommendation and your next

- You will also be advised in writing of all loan decisions.

How quickly can a loan application move to closing and loan funds be disbursed?

- Timing depends on the completeness of the

- An SBA loan officer will work with you to provide all the necessary information needed to reach a loan determination.

- The goal is to arrive at a decision on your application within 2-3 weeks.

- If approved, the SBA will prepare and send your Loan Closing Documents to you for your signature.

- Once they receive your signed Loan Closing Documents, an initial disbursement will be made to you within 5 days for Economic injury- working capital of $25,000).

- A SBA case manager will be assigned to work with you to help you meet all loan conditions.

- They will also schedule subsequent disbursements until you receive the full loan amount.

What if my circumstances change and I need more money than I originally applied for?

- Your SBA loan may be adjusted after closing due to your changing circumstances, such as increasing the loan for unexpected costs or reducing the loan due to additional insurance

- Please contact your SBA case manager for more details.

What if I have an existing SBA Disaster Loan?

- Applicants can have an existing SBA Disaster Loan and still qualify for an Economic Injury Disaster Loan for this disaster, but the loans cannot be consolidated.

What happens if a loan request is denied?

- If the loan request is denied, the applicant will be given up to six months in which to provide new information and submit a written request for reconsideration.

GABB COVID-19 Meeting April 7: Recording

Join Zoom Meeting

https://zoom.us/j/556664179?pwd=alNxa0hNREN3NytJOGRySjFKd2R0dz09

Meeting ID: 556 664 179

Password: 934001

One tap mobile

+19292056099,,556664179# US (New York)

+13126266799,,556664179# US (Chicago)

Dial by your location

+1 929 205 6099 US (New York)

+1 312 626 6799 US (Chicago)

+1 301 715 8592 US

+1 346 248 7799 US (Houston)

+1 669 900 6833 US (San Jose)

+1 253 215 8782 US

Meeting ID: 556 664 179

Password: 934001

Find your local number: https://zoom.us/u/ad549vKb9e

SBA Low-Interest Loans for Small Business Owners

As the country faces the challenges related to the Coronavirus (COVID-19), SBA lenders in the Georgia Association of Business Brokers say they are still in business, approving loans, and can provide information about the SBA’s Economic Injury Disaster Loans.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act just passed by Congress includes programs and initiatives intended to assist business owners with whatever needs they have right now. Details included at this link.

Information about available loans is changing daily, so anyone with any questions about SBA loans available should contact a GABB Affiliate lender, and GABB will try to update information here as it becomes available.

“The SBA Team at Atlantic Capital is here as a resource to help businesses access the capital they need to continue to run and grow their companies,” says Thomas Rockwood, Vice President of SBA Lending at Atlantic Capital Bank.

Atlantic Capital, Cheryl Beer, Senior Vice President of SBA Lending at the Piedmont Bank, and other GABB affiliates who are SBA lenders say are still approving new loans for borrowers and fully participating in all of the U.S. Small Business Administration (SBA) loan programs designed to assist small business owners. These valuable GABB affiliates are still providing businesses access to capital through the SBA 7a, 504, and Express loan programs, including the Veterans Advantage loans, Woman-owned business loans, and programs for minority-owned businesses.

GABB Board member Kim Eells, Senior Vice President of SBA Business Development at Georgia Primary Bank, said as of March 18, the State of Georgia has been added as a declared state for Coronavirus Disaster Loan Assistance with the SBA. Businesses that have been adversely affected by COVID-19 may now apply for Disaster Assistance directly with the SBA, no banks involved, Eells said. These loans are up to $2,000,000, up to 30 year term, fixed rate of 3.75%. Apply online at: www.sba.gov/disaster.

“I was just on a training/conference call with SBA regarding the disaster loans,” Eells said. “They are going to make it as painless and fast as possible for the borrowers. They said everyone should apply, apply, apply.”

U.S. Small Business Administration is providing low-interest federal disaster loan funds for working capital to small businesses and private, non-profit organizations suffering substantial economic injury as a result of COVID-19.

SBA’s Economic Injury Disaster Loans:

- Offer up to $2 million in assistance

- May be used to pay fixed debts, payroll, accounts payable and other bills that can’t be paid because of the

disaster’s impact - Interest rate is 3.75% for small businesses

- Interest rate for non-profits is 2.75%

- Offer terms up to a maximum of 30 years (determined on a case-by-case basis)

Ryan Stoll, Vice President SBA Banker, at Cadence Bank, provided this PDF with more details about the SBA loan program.

Webinar material-Coronavirus 03.14.20

“These funds are intended to replace lost sales or profits or for expansion for those businesses directly affected by the Covid 19 virus.,” said Susan Kite, Senior Vice President of SBA Business Development at Georgia Primary Bank. Susan has also posted information about the loans on the GABB member forum.”We are still making business acquisition loans at Georgia Primary Bank!”

For more information, please contact the SBA Disaster Assistance Customer Service Center. Call 1-800-659-2955 (TTY: 1-800-877-8339) or e-mail disastercustomerservice@sba.gov.

Carolyn Robinson, a Senior Vice President at Acclivity Financial, A Subsidiary of Citizens Bank, said her bank is helping “our borrowers who want a loan payment deferment. We are continuing to underwrite, process and close loans.”

Carolyn provided additional details about the three-step process for applying for SBA disaster loans.Three_Step_Process_SBA_Disaster_Loans

The GABB encourages small businesses to contact one of the many SBA lenders in our association because these lenders have a proven track record of successfully working with business owners.

“We hope that all of you stay safe and healthy in the coming weeks and months,” said David Brindley, Vice President of Live Oak Bank. “Together, we will get through this challenging time!”

Read More

The Silver Lining in the Coronavirus: Think Positive!

Photo by Skitterphoto from Pexels

By Dean Burnette, GABB President and managing broker of Best Business Brokers of Savannah

In the last few days my email has had a growing amount of Covid-19 Update emails! When I turn the television or radio on I hear or see “Corona virus” 100’s of times. Although coverage of a global pandemic is understandable, we’re only human.

If exposure to the virus doesn’t get us, hearing bad news may.

Being an eternal optimist with real life experience through several world economic cycles, including the oil embargo of the 1970’s and 1980’s, The Y-2-K threat of 2000, the real estate bubble, I’m quite confident that most of us will survive this. In fact, some will prosper and some will not.

There will be short term challenges. I have been personally impacted by the current travel challenges. One buyer was supposed to fly in from Chicago last week to look at a business, another client was supposed to fly down from Ohio, and they both had to cancel. I’m expecting a buyer from New York to fly into Savannah Saturday morning, and I’m wondering if he will actually make it?

Some will be impacted more than others; I hope we will be compassionate and aware of other’s struggles. As in the past, most people will come out the other side of this challenge better than they imagined. In each of these cycles, new industries were created!

New industries will be created; some will become obsolete.

We’ve all learned a new term with Covid-19, Social Distancing. I’ve long said that there are some people you have to love from a distance, and social distancing certainly puts a new spin on that! The world may never be the same again.

I am over 60, and so I am at a higher risk than the general population and should take extra precautions. With all the technological advances in communication and social media, I don’t know whether to feel safer or more vulnerable with my higher risk senior status. But I do know that in every crisis, there are possibilities, a silver lining in a rain cloud.

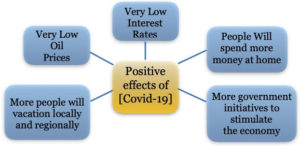

The positive side of the Covid-19 experience

This too shall pass and probably sooner than we imagine! The world is much better equipped to overcome pandemics and other challenges that come at us. We are currently witnessing in real time the wonders of technology and the benefits we have in this day and time.

Instead of dwelling on the negative aspects of our current world challenges, we can find the silver lining. For example, I have two clients who have been able to secure business loans because of the lowered interest rates. After being cooped up for a couple of weeks or longer I believe people will fill up their gas tanks with cheap gas and travel locally, spend money in small businesses. I hope we can use this time of solitude to appreciate our families more and get some of those closets, garages, or spring cleaning done.

Opportunities will emerge

Other bright spots:

Other bright spots:

- Gasoline prices are very low.

- Interest rates are at historic lows, creating many opportunities for economic growth through new manufacturing opportunities and business expansion.

- Instead of going on cruises and traveling to other countries, people will fill up their tanks and spend their money locally in small businesses. More people will drive to Savannah or visit the Atlanta Aquarium!

- Many companies are encouraging people to work from home during the crisis, and after the crisis many will continue working from home.

- We all have learned the best way to wash our hands, and we’re washing more frequently, and most of us will be more aware of our health and hygiene.

- Because of our new awareness of how much we depend on foreign companies for vital products, more manufacturing will be done here.

- New industries will be created and more jobs and business opportunities will result from this crisis.

If you have been considering buying or selling a business, the stars are lining up, interest rates are low, and the U.S. government will be putting extra efforts into economic stimulus. Gas prices are very low, and people will have more money to spend in local businesses. The list goes on. If you have been waiting for the right time to buy or sell a business, that time is now. It sometimes takes months to close a deal, by that time the virus will be history, and businesses will beginning to flourish again!

Read More

“Irksome Geopolitical Concerns” Are Potential Curveballs to 2020 Economic Growth Prospects

ATLANTA–Having the Federal Reserve on hold for the foreseeable future, bipartisan agreement on fiscal spending and the signed phase one tariff deal with China have reduced the uncertainty that typically bedevil growth prospects, according to Rajeev Dhawan of the Economic Forecasting Center at Georgia State University’s Robinson College of Business.

ATLANTA–Having the Federal Reserve on hold for the foreseeable future, bipartisan agreement on fiscal spending and the signed phase one tariff deal with China have reduced the uncertainty that typically bedevil growth prospects, according to Rajeev Dhawan of the Economic Forecasting Center at Georgia State University’s Robinson College of Business.

“The seeds for 2020 growth were sown last year,” Dhawan wrote in his “Forecast of the Nation,” released Feb. 26, 2020. “In early 2019, business investment was already waning (after the boost from the Dec. 2017 tax reforms) when it hit a few potholes.”

Those potholes were the shocks of a sharp drop in oil prices and the grounding of Boeing’s 737 MAX, causing a contraction in business spending by late 2019.

“The die was cast for a growth slowdown in 2020,” Dhawan said.

The typical economic pullback experienced during a presidential election year began earlier than usual this cycle when election rhetoric heated up ahead of when expected.

Dhawan posits that subpar GDP growth (1.6 percent) in the first half of 2020 will be followed by a ramped-up GDP of 2.0 percent in the year’s second half due to a “positive exigent circumstance” when the 737 MAX returns to the skies in mid-to-late summer – tempering the impact of the ongoing presidential cycle slowdown.

Potential curveballs could beset Dhawan’s baseline forecast, the most obvious being a delayed return of the 737 MAX.

The forecaster is more concerned about what he described as “irksome geopolitical concerns” – e.g., Middle East flare-ups affecting oil production and capacity, kinks in the trade deal with China, post-Brexit uncertainty in EU-UK relations, action on past threats about German auto exports, and COVID-19, the coronavirus that first appeared in late 2019 in Hubei province, China, which Dhawan said is “the biggest threat to the 2020 forecast.

“At present, the key issue for us the incidence of spread of the virus outside China, and the Chinese have taken steps to limit it,” Dhawan said. “But, unlike a finite event, such as a hurricane or earthquake, the coronavirus is still playing out, making it hard to assess economic impact.”

The biggest economic problem now, according to Dhawan, is that factory workers are stuck at home after the Chinese New Year holiday.

“China is a vital part of the world’s supply chain for goods ranging from toys to iPhones. For an economic impact to happen, this disruption would need to last awhile, say until mid-April. When inventories run out, what will Amazon sell here? What will Apple and Samsung do?” Dhawan asked. “This is what I worry about the most.”

Highlights from the Economic Forecasting Center’s National Report

- Overall GDP growth will be 1.8 percent in 2020, 2.0 percent in 2021 and 1.7 percent in 2022.

- Investment growth will be only 0.6 percent in 2020, 4.3 percent in 2021 and 3.6 percent in 2022. Monthly job gains will be 143,000 in 2020, drop to 104,200 in 2021 and a similar 94,400 in 2022.

- Housing starts will average 1.258 million in 2020, 1.224 million in 2021 and 1.234 million in 2022. Vehicle sales will average 16.3 million in 2020, and 16.0 million in 2021 and 2022.

- The 10-year bond rate will average 1.9 percent in 2020, 2.7 percent in 2021 and 3.0 percent in 2022.