Buying A Small Business: Earnest Money Deposits Should Be Reasonable

By Peter Siegel MBA, BizBen Founder, ProBuy, ProSell, ProIntermediary Programs

I was speaking with a prospective business buyer the other day – he had just signed up to get business purchase financing. He said he wanted the business; however, he was uncomfortable putting down a 10% deposit for a $350,000 business. He asked if he could lower the deposit requirement to $5,000.

I asked a business broker that day on the phone what his opinion was on earnest money deposits for escrow/bulk sale accounts when selling a small business, here is what he told me via email:

Earnest money deposits serve two purposes.

First, they show the seller that you are serious about buying the business. Secondly, in the event that you as the buyer default on the purchase agreement after due diligence and other contingencies have been removed, the earnest money deposit typically serves as liquidated damages to the seller. Would you as a business owner take an offer for your $350,000 business seriously when it was accompanied by a good faith deposit of only $5,000? Would you allow someone to tie up your business for 30, 45, 60 days or more with only $5,000 in escrow?

Occasionally a buyer will write an offer, provide a 10% deposit check and then ask that it be held for two to four weeks or more until all contingencies have been removed. A good faith deposit that can’t be deposited is no good faith at all. The contingencies in a purchase agreement protect you as the buyer, and if you walk away from the transaction before the contingencies have been released, your deposit will be returned to you less any escrow costs incurred. It is your good faith deposit that is supposed to help protect the seller in the transaction. If the check can’t be deposited then what good is it? The buyer is literally asking to tie up the seller’s business for two to four weeks or more with nothing.

The basic rule is this – When there is no money, there is no Buyer.

A 10% deposit shows good faith, shows your intent to purchase the business, and separates the buyers from the shoppers.

Buying a business is a serious process, and offers should not be made lightly. If you don’t know enough about the business to be confident enough to put down a 10% deposit, continue your research until you are more confident. When you are ready to make an offer, show the seller you are serious about buying his/her business. You will find that your offer will be more readily accepted when it is accompanied by a standard 10% deposit.

If you really want to stand out above the rest, provide a cashiers check for the deposit. Then you truly have shown the Owner/Seller your intention to buy their small business is serious.

Orange County, Calif., business broker Joe Ranieri, said “the minimum I want to see when opening escrow is $10,000. Anything less and I feel the buyer is not showing enough commitment. Granted, we all know that a buyer can invent any reason for canceling an escrow, and possibly get a percentage of the deposit back, but $10,000 shows good faith.”

If the purchase price is north of $200,000-$250,000, Ranieri said he would encourage the seller to ask for a greater amount for the security deposit. “I remind the buyer, that from the seller’s perspective, that once we open escrow, the business is basically off the market, unlike selling a house which can accumulate many back up offers, but with a business, many buyers will simply look somewhere else once it’s in escrow.”

San Francisco business broker Timothy Cunha said the “good faith refundable deposit” is often the major impediment to an offer being made and accepted. “And it should be – neither the buyer nor the seller is benefited by a half-hearted mediocre interest in the business,” he said.

A properly drafted contract will stipulate that the deposit go to an independent escrow agent and to be fully refundable if the purchaser terminates the contract prior to the end of due diligence “for any reason or for no reason.” Cunha says he “will only use an escrow agent who will charge no escrow fee until due diligence has expired and they actually begin their work.”

The deposit is important because “once the business goes into contract, the business is effectively off the market; it cannot be shown and no other offer can be accepted,” Cunha says. “The seller has to know the buyer is serious before shutting down the marketing “funnel.” ”

“If the buyer can’t raise 10% of the purchase price for a deposit, it is highly unlikely that he or she has the requisite cash to be a serious prospective purchaser of the business,” he said. “And, the deposit should be substantial enough to signify the commitment of the buyer – 10% is a good number that seems to work for most deals under a half million dollars; for higher purchase prices, sometimes a deposit between 5% and 10% can be negotiated.”

This article originally appeared on the BizBen blog.

Read More

Building a Strong Brand: What Do Your Customers Say About YOU?

What do your customers/clients say about your or your company when you’re not around?

What do the employees say about you or your company when you’re not around?

Those things represent your external and internal brands, says brand guru Skot Waldron, and they can help or hurt you. Waldron spoke on June 30 to the Georgia Association of Business Brokers about building brand loyalty.

At the end of the day, we all crave loyalty, Waldron says. We want loyalty from our family members, loyalty from our customers, loyalty from employees, and loyalty from the companies we dedicate ourselves to. Your brand is typically associated with how you appear on the outside and how you communicate your value to the world. Skot pushes this idea by saying your brand starts on the inside and drives what’s on the outside.

Things that hurt your internal brand:

- Generic vision/mission/values that inspires no one.

- No self-awareness.

- Fear/manipulation

- Passive aggressiveness

- Misalignment

- You aren’t consistent in your communication.

You damage your external brand by:

- Treating marketing as an expense vs. an investment.

- Staying busy with day-to-day tactics instead of focusing on a strategy.

- Not differentiating your product or service.

- Not knowing how to clearly and confidently talk about your product or service.

- Being inconsistent and lacking a cohesive message

that resonates with people.

Skot recommends that entrepreneurs and small business people should ask trusted colleagues these questions: What five words would you use to

describe me/my business? What are my/our top 3 strengths? What are my/our top 3 weaknesses?

Listen to Skot’s presentation here.

Skot’s PPT Presentation “Why People Aren’t Loyal to Your Brand & What to Do About It,” is linked here:Why People Aren’t Loyal to Your Brand

For the past 18 years, Skot Waldron’s brand work for clients such as J.P. Morgan Chase, CDC, Georgia Tech, Royal Caribbean, Sesame Workshop, Chiquita, and The Coca-Cola Company has included both employee-centric and customer-centric projects.

He helps organizations communicate more effectively with their employees and customers with the goal of creating more alignment, consistency, and loyalty. Skot believes you have to be healthy on the inside (culture) in order to truly be healthy on the outside (brand and marketing). He helps with both.

In addition to running his own coaching and creative agency, Skot has been teaching brand development at the Miami Ad School in Atlanta. He has also traveled to different cities in the U.S. to conduct communication training and speaks about how the value of branding pertains to us as individuals, teams, families, and businesses.

The Georgia Association of Business Brokers, the state’s largest and most prominent association of professionals dedicated to the purchase and sale of businesses and franchises, is holding brief weekly meetings online during the pandemic. Business brokers, bankers, business attorneys and other professionals join the weekly calls to ask and answer questions about buying and selling a business during the pandemic. The GABB also maintains a listing service with hundreds of Georgia businesses for sale.

To join the GABB’s Tuesday meetings, please go to

https://us02web.zoom.us/j/95506520094?pwd=WXdtNjhQVmRSWWdDNk5nV2lHZnNKdz09

Meeting ID: 955 0652 0094

Password: 054703

Documenting Material Adverse Changes: Selling a Business in the Pandemic

The COVID-19 pandemic has had a significant effect on all U.S. businesses, but that doesn’t mean the owners won’t be able to sell.

Thomas Rockwood, Vice President of SBA Lending at Atlantic Capital Bank, outlined for the Georgia Association of Business Brokers what documents business sellers should prepare if they are anticipating selling their business in the near future. Rockwood spoke to a virtual GABB meeting on June 23, 2020.

The pandemic could affect any pending contract because it constitutes a Material Adverse Change (abbreviated MAC), material adverse event (MAE), or material adverse effect (also MAE). In other words, changes triggered by COVID-19 COULD significantly reduce a company’s value because it could impact how the company operates in the future. Many contracts to acquire, invest in, or lend money to a company contain a term that allows the acquirer, investor, or lender to cancel the transaction if a material adverse change occurs and does directly affect SBA Eligibility for a loan.

The pandemic could affect any pending contract because it constitutes a Material Adverse Change (abbreviated MAC), material adverse event (MAE), or material adverse effect (also MAE). In other words, changes triggered by COVID-19 COULD significantly reduce a company’s value because it could impact how the company operates in the future. Many contracts to acquire, invest in, or lend money to a company contain a term that allows the acquirer, investor, or lender to cancel the transaction if a material adverse change occurs and does directly affect SBA Eligibility for a loan.

“A material adverse change can happen to anybody at any time,” Rockwood noted. It’s critical for business owners to document how the event affected their business in order to borrow SBA funds and obtain a favorable purchase price.

When collecting sellers’ financials, SBA lenders will want to see:

- Last 3 years Filed Business Tax Returns

- 2019 FYE Financials to include

- P&L, Balance Sheet, AR & AP Aging Report & Debt Schedule

- 2020 YTD Financials to include

- P&L, Balance Sheet, AR & AP Aging Report & Debt Schedule

“We’re in this place where we have no idea what tomorrow looks like,” Rockwood said. “What are the things we can control?”

A seller can document the impact of the pandemic or other MAE on their business by showing month-by-month P&L comparisons. Did the seller’s business bounce back in June? Another helpful strategy would be identifying sales by customer, showing key customers and how they were affected by the MAE. Sales by product could also be beneficial, Rockwood said.

Preparing a memo of understanding could help a buyer, Rockwood said, because it describes in detail what is going on with a business. For example, if sales go up, but net profits go down, what happened? A memo could explain that labor costs rose and the business had to hire more people to move the product out the door.

If a seller can “bookend the start and end of MAC,” that’s going to help paint a strong picture for a business buyer on what happened to the business, Rockwood said.

Sellers ought to come up with a playbook of operations of how the business has or plans to keep employees safe, so that a potential buyer can walk in and continue running the business smoothly. Although some sellers stay on and advise buyers, sometimes they don’t. That playbook will help a new owner because it “outlines what the seller did, how they handled the situation, and gives some advice to the new buyer.”

“It’s the seller’s company, and they know it better than anybody else could,” Rockwood said. “That will be very beneficial to any buyers who want to buy a business.”

A video recording of the meeting is linked here.

Mr. Rockwood’s presentation is available here.

Preparing to Sell After the Pandemic

Mr. Rockwood has spent more than 16 years working with companies to provide government guaranteed lending solutions. He has a B.S. in Marketing & Business from Central Washington University; and an M.B.A. in Marketing Management, Regis University.In addition to being a GABB member, Mr. Rockwood is an executive board member of the Georgia Lenders Quality Circle (GLQC) and a member of the National Association of Government Guaranteed Lenders (NAGGL).

The Georgia Association of Business Brokers, the state’s largest and most prominent association of professionals dedicated to the purchase and sale of businesses and franchises, is holding brief weekly meetings online during the pandemic. Business brokers, bankers, business attorneys and other professionals join the weekly calls to ask and answer questions about buying and selling a business during the pandemic.

To join the GABB’s Tuesday meetings, please go to

https://us02web.zoom.us/j/95506520094?pwd=WXdtNjhQVmRSWWdDNk5nV2lHZnNKdz09

Meeting ID: 955 0652 0094

Password: 054703

Read More

Negotiating the Price Gap Between Buyers and Sellers

Sellers generally desire all-cash transactions; however, oftentimes partial seller financing is necessary in typical middle market company transactions. Furthermore, sellers who demand all-cash deals typically receive a lower purchase price than they would have if the deal were structured differently.

Although buyers may be able to pay all-cash at closing, they often want to structure a deal where the seller has left some portion of the price on the table, either in the form of a note or an earnout. Deferring some of the owner’s remuneration from the transaction will provide leverage in the event that the owner has misrepresented the business. An earnout is a mechanism to provide payment based on future performance. Acquirers like to suggest that, if the business is as it is represented, there should be no problem with this type of payout. The owner’s retort is that he or she knows the business is sound under his or her management but does not know whether the buyer will be as successful in operating the business.

Moreover, the owner has taken the business risk while owning the business; why would he or she continue to be at risk with someone else at the helm? Nevertheless, there are circumstances in which an earnout can be quite useful in recognizing full value and consummating a transaction. For example, suppose that a company had spent three years and vast sums developing a new product and had just launched the product at the time of a sale. A certain value could be arrived at for the current business, and an earnout could be structured to compensate the owner for the effort and expense of developing the new product if and when the sales of the new product materialize. Under this scenario, everyone wins.

The terms of the deal are extremely important to both parties involved in the transaction. Many times the buyers and sellers, and their advisors, are in agreement with all the terms of the transaction, except for the price. Although the variance on price may seem to be a “deal killer,” the price gap can often be resolved so that both parties can move forward to complete the transaction.

Listed below are some suggestions on how to bridge the price gap:

- If the real estate was originally included in the deal, the seller may choose to rent the premise to the acquirer rather than sell it outright. This will decrease the price of the transaction by the value of the real estate. The buyer might also choose to pay higher rent in order to decrease the “goodwill” portion of the sale. The seller may choose to retain the title to certain machinery and equipment and lease it back to the buyer.

- The purchaser can acquire less than 100% of the company initially and have the option to buy the remaining interest in the future. For example, a buyer could purchase 70% of the seller’s stock with an option to acquire an additional 10% a year for three years based on a predetermined formula. The seller will enjoy 30% of the profits plus a multiple of the earnings at the end of the period. The buyer will be able to complete the transaction in a two-step process, making the purchase easier to accomplish. The seller may also have a “put” which will force the buyer to purchase the remaining 30% at some future date.

- A subsidiary can be created for the fastest growing portion of the business being acquired. The buyer and seller can then share 50/50 in the part of the business that was “spun-off” until the original transaction is paid off.

- A royalty can be structured based on revenue, gross margins, EBIT, or EBITDA. This is usually easier to structure than an earnout.

- Certain assets, such as automobiles or non-business-related real estate, can be carved out of the sale to reduce the actual purchase price.

Although the above suggestions will not solve all of the pricing gap problems, they may lead the participants in the necessary direction to resolve them. The ability to structure successful transactions that satisfy both buyer and seller requires an immense amount of time, skill, experience, and most of all – imagination.

The post Negotiating the Price Gap Between Buyers and Sellers appeared first on Deal Studio – Automate, accelerate and elevate your deal making.

Pandemic Will Impact Business Valuations

The COVID-19 pandemic is going to affect the valuation of businesses, and professionals are likely to take into account a wider number of factors when determining the fair market value of a business.

That’s what two business valuation experts told the Georgia Association of Business Brokers in a conference call on Tuesday, May 26. Dan Browning is the founder and President of DB Consulting, Inc. and David H. Hern, CPA/ABV, ASA, CEPA, a financial analyst with Sofer Advisors spoke to the GABB online. View the conference online here.

“The biggest issue is uncertainty, which heightens the risk, and higher risk leads to lower value,” Browning said. People who assign values to businesses are, by their nature, trying to predict future business conditions, which is tricky anytime, but particularly now. While many businesses have suffered, some businesses “have gone gangbusters,” Browning said. The cost of capital has actually gone down for some businesses, specifically those that have been able to obtain SBA-backed assistance in the form of grants or low-interest loans.

However, some valuation clients are “taking advantage of uncertainty,” Hern said. Some clients are using this time to “do tricky estate planning, issue equity grants, possibly get values frozen below normal,” he said.

If a business valuation was triggered before the onset of the pandemic in the US, some will argue it’s a subsequent event, and should not affect the pre-crisis value. Browning said he has started including an appendix, a disclaimer, calling COVID-19 a subsequent event, which didn’t affect value as of the valuation date.

Browning shared a timeline from respected business valuation expert Jim Hitchner who tracks the impact of the virus on various markets.

Hern shared a Sofer analysis of the mobility of the U.S. Market Mobility of US Market Sofer document

Restaurants have been seriously impacted by the crisis, and many are trying to decide whether it’s worth reopening. Some, like pizza restaurants, have adapted better to a takeout model.

Restaurant broker Dominique Maddox said many of his clients are opting not to reopen and are trying to sell their assets and get out from a multi-year lease. Pizza concepts were able to keep going strong, Maddox said.

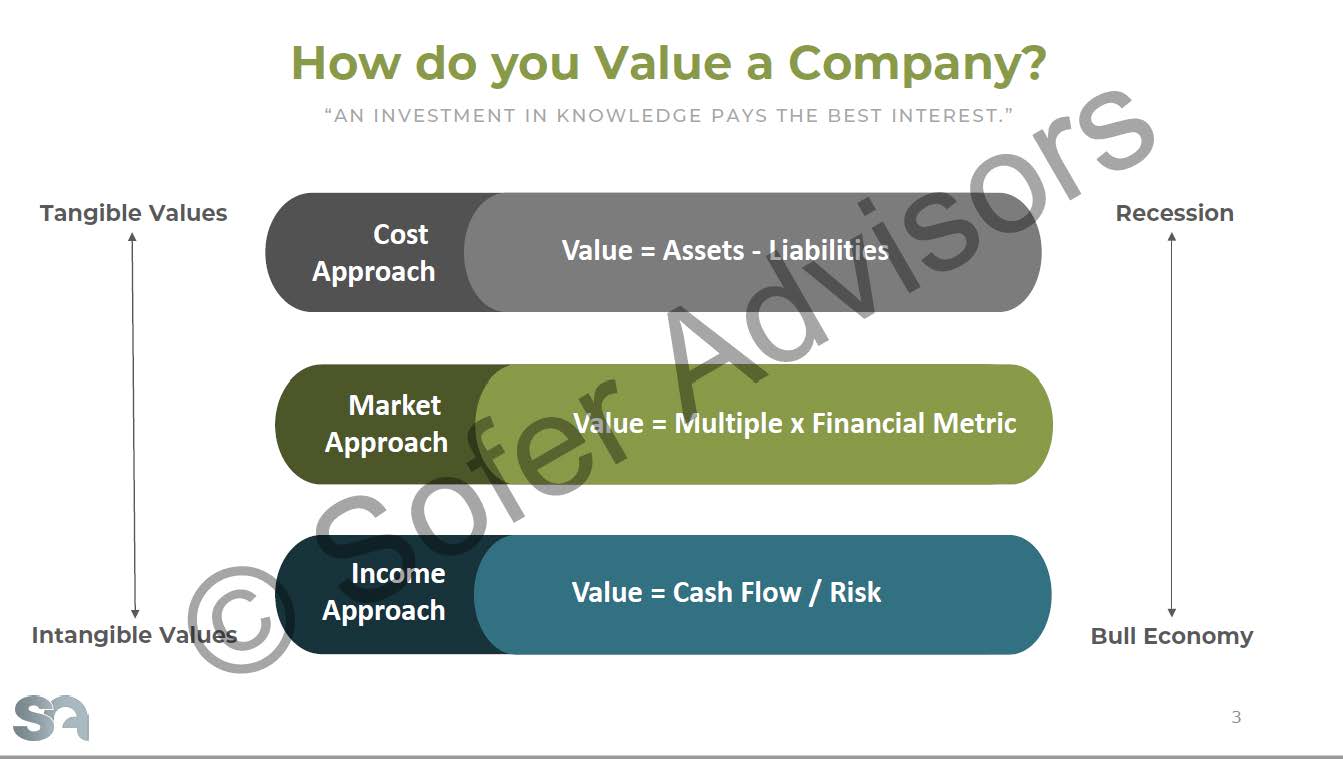

Hern cited three approaches to business valuation: Cost Approach, in which the value of the business is equal to their assets minus liabilities. The Market Approach determines the value of a business based on a multiple and a financial metric. The Income Approach sets the value at cash flow divided by risk.

Hern cited three approaches to business valuation: Cost Approach, in which the value of the business is equal to their assets minus liabilities. The Market Approach determines the value of a business based on a multiple and a financial metric. The Income Approach sets the value at cash flow divided by risk.

The methods skew towards tangible values during a recession, and during bull economy tends to more intangible values. Hern says he’s been running a variety of scenarios taking into account whether the economic recovery may be V-shaped, U-shaped or something else. Browning predicted a W-shaped recovery, with ups and downs.

Businesses may be getting valuations that specify a range of values instead of a single value, Browning said.

“It’s important not to get too negative,” Browning said. “There is a going to be a recovery, there is going to be coming out of all of this.” The recovery may be bumpy, but it will come.

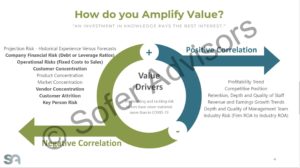

Hern is recommending that business owners prepare their businesses to be in the best shape for the future, fixing problems. You can amplify value by reducing the customer concentration, reducing debt, improving their competitive position, improving staff depth and retention, etc.

“Companies that have fixed these types of issues will sell for better value,” Hern said.

Hern said he will be looking at vendor concentration in the future when valuing a business.

“Doing business is going to be more expensive going forward,” said Browning. Businesses are going to have to buy extra cleaning supplies, extra protective gear, more training of employees.

Hern’s presentation: GABB Sofer

Dan Browning is the founder and President of DB Consulting, Inc. His credentials include:

Dan Browning is the founder and President of DB Consulting, Inc. His credentials include:

- Master Analyst in Financial Forensics (MAFF) from the National Association of Certified Valuators and Analysts, originally awarded August 1999

- Accredited in Business Appraisal Review (ABAR) from the National Association of Certified Valuators and Analysts, originally awarded March 2010

- Georgia Association of Business Brokers (Affiliate Member)

- State Bar of Georgia (Active Member; Eminent Domain and Nonprofit Law Section Memberships)

- Editorial Board, Business Appraisal Practice (IBA Journal) 2013-2015

- University of Notre Dame, Master of Arts (Government), January 1995

- Emory University School of Law, Juris Doctor, May 1992

- Emory University, Bachelor of Arts, May 1985; Phi Beta Kappa

David H. Hern, CPA/ABV, ASA, CEPA, is a highly qualified financial analyst with Sofer Advisors.He has exceptional credentials in determining the true, comprehensive value of an organization. In addition, he has something even more rare: a proven ability to simply and clearly communicate analysis to boards of directors, legal and financial advisors, Company management (CEOs, CFOs, controllers, etc.) and private equity portfolio managers. Mr. Hern offers litigation assistance, estate and tax planning, and business enterprise valuations for various privately-held and public companies. He has been recognized for enabling organizations to determine their enterprise and equity value for a variety of situations

David H. Hern, CPA/ABV, ASA, CEPA, is a highly qualified financial analyst with Sofer Advisors.He has exceptional credentials in determining the true, comprehensive value of an organization. In addition, he has something even more rare: a proven ability to simply and clearly communicate analysis to boards of directors, legal and financial advisors, Company management (CEOs, CFOs, controllers, etc.) and private equity portfolio managers. Mr. Hern offers litigation assistance, estate and tax planning, and business enterprise valuations for various privately-held and public companies. He has been recognized for enabling organizations to determine their enterprise and equity value for a variety of situations

Education

- Georgia Institute of Technology, Scheller College of Business, Atlanta GA. Masters of Business Administration, Finance emphasis.

- Georgia Institute of Technology, Scheller College of Business, Atlanta, GA. Bachelors of Science, Management with Accounting emphasis.

Certifications

- Certified Public Accountant (CPA) — State of Georgia

- Accredited in Business Valuation (ABV)

- Accredited Senior Appraiser (ASA)

- Certified Exit Planning Advisor (CEPA)

Read More