Where Did the Cash Go? Add-Backs to Consider When Buying a Business

Accountants routinely assist business owners to help accomplish the goal of minimizing taxes. But, to truly understand the value of the business and accurately project future cash flow, it is important to look beyond the tax returns to realize how the money is being spent.

Dave Chambless has extensive experience in business development; finance; operations; sales; marketing; and international channel development and management. Mr. Chambless has a Master of Business Administration in Finance degree from the Wharton School of the University of Pennsylvania and a Bachelor of Industrial and Systems Engineering degree from Georgia Tech. He has regularly been among the top-selling business brokers honored by the GABB’s annual Million-Dollar Club.

Dave Chambless has extensive experience in business development; finance; operations; sales; marketing; and international channel development and management. Mr. Chambless has a Master of Business Administration in Finance degree from the Wharton School of the University of Pennsylvania and a Bachelor of Industrial and Systems Engineering degree from Georgia Tech. He has regularly been among the top-selling business brokers honored by the GABB’s annual Million-Dollar Club.

Documenting Material Adverse Changes: Selling a Business in the Pandemic

The COVID-19 pandemic has had a significant effect on all U.S. businesses, but that doesn’t mean the owners won’t be able to sell.

Thomas Rockwood, Vice President of SBA Lending at Atlantic Capital Bank, outlined for the Georgia Association of Business Brokers what documents business sellers should prepare if they are anticipating selling their business in the near future. Rockwood spoke to a virtual GABB meeting on June 23, 2020.

The pandemic could affect any pending contract because it constitutes a Material Adverse Change (abbreviated MAC), material adverse event (MAE), or material adverse effect (also MAE). In other words, changes triggered by COVID-19 COULD significantly reduce a company’s value because it could impact how the company operates in the future. Many contracts to acquire, invest in, or lend money to a company contain a term that allows the acquirer, investor, or lender to cancel the transaction if a material adverse change occurs and does directly affect SBA Eligibility for a loan.

The pandemic could affect any pending contract because it constitutes a Material Adverse Change (abbreviated MAC), material adverse event (MAE), or material adverse effect (also MAE). In other words, changes triggered by COVID-19 COULD significantly reduce a company’s value because it could impact how the company operates in the future. Many contracts to acquire, invest in, or lend money to a company contain a term that allows the acquirer, investor, or lender to cancel the transaction if a material adverse change occurs and does directly affect SBA Eligibility for a loan.

“A material adverse change can happen to anybody at any time,” Rockwood noted. It’s critical for business owners to document how the event affected their business in order to borrow SBA funds and obtain a favorable purchase price.

When collecting sellers’ financials, SBA lenders will want to see:

- Last 3 years Filed Business Tax Returns

- 2019 FYE Financials to include

- P&L, Balance Sheet, AR & AP Aging Report & Debt Schedule

- 2020 YTD Financials to include

- P&L, Balance Sheet, AR & AP Aging Report & Debt Schedule

“We’re in this place where we have no idea what tomorrow looks like,” Rockwood said. “What are the things we can control?”

A seller can document the impact of the pandemic or other MAE on their business by showing month-by-month P&L comparisons. Did the seller’s business bounce back in June? Another helpful strategy would be identifying sales by customer, showing key customers and how they were affected by the MAE. Sales by product could also be beneficial, Rockwood said.

Preparing a memo of understanding could help a buyer, Rockwood said, because it describes in detail what is going on with a business. For example, if sales go up, but net profits go down, what happened? A memo could explain that labor costs rose and the business had to hire more people to move the product out the door.

If a seller can “bookend the start and end of MAC,” that’s going to help paint a strong picture for a business buyer on what happened to the business, Rockwood said.

Sellers ought to come up with a playbook of operations of how the business has or plans to keep employees safe, so that a potential buyer can walk in and continue running the business smoothly. Although some sellers stay on and advise buyers, sometimes they don’t. That playbook will help a new owner because it “outlines what the seller did, how they handled the situation, and gives some advice to the new buyer.”

“It’s the seller’s company, and they know it better than anybody else could,” Rockwood said. “That will be very beneficial to any buyers who want to buy a business.”

A video recording of the meeting is linked here.

Mr. Rockwood’s presentation is available here.

Preparing to Sell After the Pandemic

Mr. Rockwood has spent more than 16 years working with companies to provide government guaranteed lending solutions. He has a B.S. in Marketing & Business from Central Washington University; and an M.B.A. in Marketing Management, Regis University.In addition to being a GABB member, Mr. Rockwood is an executive board member of the Georgia Lenders Quality Circle (GLQC) and a member of the National Association of Government Guaranteed Lenders (NAGGL).

The Georgia Association of Business Brokers, the state’s largest and most prominent association of professionals dedicated to the purchase and sale of businesses and franchises, is holding brief weekly meetings online during the pandemic. Business brokers, bankers, business attorneys and other professionals join the weekly calls to ask and answer questions about buying and selling a business during the pandemic.

To join the GABB’s Tuesday meetings, please go to

https://us02web.zoom.us/j/95506520094?pwd=WXdtNjhQVmRSWWdDNk5nV2lHZnNKdz09

Meeting ID: 955 0652 0094

Password: 054703

Read More

Pandemic Will Impact Business Valuations

The COVID-19 pandemic is going to affect the valuation of businesses, and professionals are likely to take into account a wider number of factors when determining the fair market value of a business.

That’s what two business valuation experts told the Georgia Association of Business Brokers in a conference call on Tuesday, May 26. Dan Browning is the founder and President of DB Consulting, Inc. and David H. Hern, CPA/ABV, ASA, CEPA, a financial analyst with Sofer Advisors spoke to the GABB online. View the conference online here.

“The biggest issue is uncertainty, which heightens the risk, and higher risk leads to lower value,” Browning said. People who assign values to businesses are, by their nature, trying to predict future business conditions, which is tricky anytime, but particularly now. While many businesses have suffered, some businesses “have gone gangbusters,” Browning said. The cost of capital has actually gone down for some businesses, specifically those that have been able to obtain SBA-backed assistance in the form of grants or low-interest loans.

However, some valuation clients are “taking advantage of uncertainty,” Hern said. Some clients are using this time to “do tricky estate planning, issue equity grants, possibly get values frozen below normal,” he said.

If a business valuation was triggered before the onset of the pandemic in the US, some will argue it’s a subsequent event, and should not affect the pre-crisis value. Browning said he has started including an appendix, a disclaimer, calling COVID-19 a subsequent event, which didn’t affect value as of the valuation date.

Browning shared a timeline from respected business valuation expert Jim Hitchner who tracks the impact of the virus on various markets.

Hern shared a Sofer analysis of the mobility of the U.S. Market Mobility of US Market Sofer document

Restaurants have been seriously impacted by the crisis, and many are trying to decide whether it’s worth reopening. Some, like pizza restaurants, have adapted better to a takeout model.

Restaurant broker Dominique Maddox said many of his clients are opting not to reopen and are trying to sell their assets and get out from a multi-year lease. Pizza concepts were able to keep going strong, Maddox said.

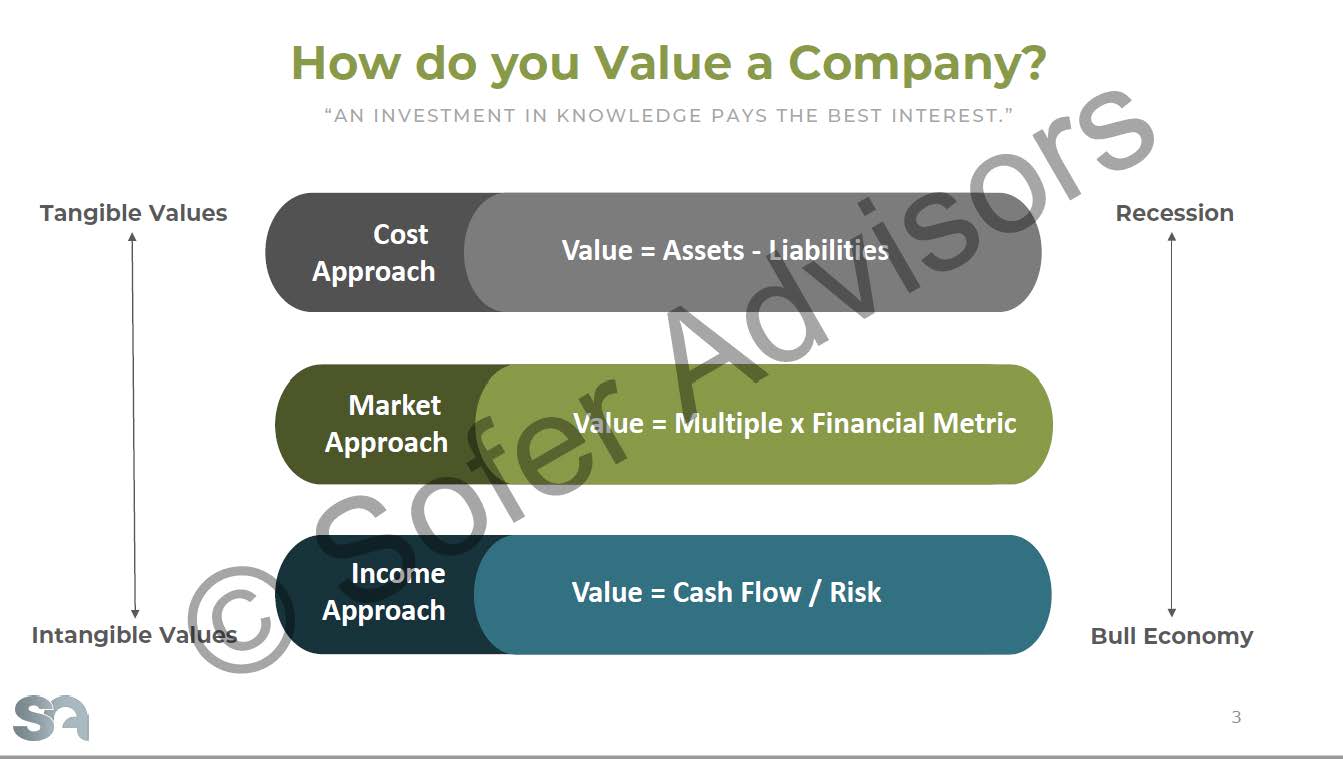

Hern cited three approaches to business valuation: Cost Approach, in which the value of the business is equal to their assets minus liabilities. The Market Approach determines the value of a business based on a multiple and a financial metric. The Income Approach sets the value at cash flow divided by risk.

Hern cited three approaches to business valuation: Cost Approach, in which the value of the business is equal to their assets minus liabilities. The Market Approach determines the value of a business based on a multiple and a financial metric. The Income Approach sets the value at cash flow divided by risk.

The methods skew towards tangible values during a recession, and during bull economy tends to more intangible values. Hern says he’s been running a variety of scenarios taking into account whether the economic recovery may be V-shaped, U-shaped or something else. Browning predicted a W-shaped recovery, with ups and downs.

Businesses may be getting valuations that specify a range of values instead of a single value, Browning said.

“It’s important not to get too negative,” Browning said. “There is a going to be a recovery, there is going to be coming out of all of this.” The recovery may be bumpy, but it will come.

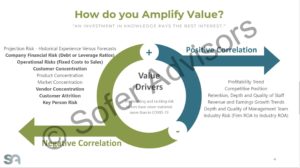

Hern is recommending that business owners prepare their businesses to be in the best shape for the future, fixing problems. You can amplify value by reducing the customer concentration, reducing debt, improving their competitive position, improving staff depth and retention, etc.

“Companies that have fixed these types of issues will sell for better value,” Hern said.

Hern said he will be looking at vendor concentration in the future when valuing a business.

“Doing business is going to be more expensive going forward,” said Browning. Businesses are going to have to buy extra cleaning supplies, extra protective gear, more training of employees.

Hern’s presentation: GABB Sofer

Dan Browning is the founder and President of DB Consulting, Inc. His credentials include:

Dan Browning is the founder and President of DB Consulting, Inc. His credentials include:

- Master Analyst in Financial Forensics (MAFF) from the National Association of Certified Valuators and Analysts, originally awarded August 1999

- Accredited in Business Appraisal Review (ABAR) from the National Association of Certified Valuators and Analysts, originally awarded March 2010

- Georgia Association of Business Brokers (Affiliate Member)

- State Bar of Georgia (Active Member; Eminent Domain and Nonprofit Law Section Memberships)

- Editorial Board, Business Appraisal Practice (IBA Journal) 2013-2015

- University of Notre Dame, Master of Arts (Government), January 1995

- Emory University School of Law, Juris Doctor, May 1992

- Emory University, Bachelor of Arts, May 1985; Phi Beta Kappa

David H. Hern, CPA/ABV, ASA, CEPA, is a highly qualified financial analyst with Sofer Advisors.He has exceptional credentials in determining the true, comprehensive value of an organization. In addition, he has something even more rare: a proven ability to simply and clearly communicate analysis to boards of directors, legal and financial advisors, Company management (CEOs, CFOs, controllers, etc.) and private equity portfolio managers. Mr. Hern offers litigation assistance, estate and tax planning, and business enterprise valuations for various privately-held and public companies. He has been recognized for enabling organizations to determine their enterprise and equity value for a variety of situations

David H. Hern, CPA/ABV, ASA, CEPA, is a highly qualified financial analyst with Sofer Advisors.He has exceptional credentials in determining the true, comprehensive value of an organization. In addition, he has something even more rare: a proven ability to simply and clearly communicate analysis to boards of directors, legal and financial advisors, Company management (CEOs, CFOs, controllers, etc.) and private equity portfolio managers. Mr. Hern offers litigation assistance, estate and tax planning, and business enterprise valuations for various privately-held and public companies. He has been recognized for enabling organizations to determine their enterprise and equity value for a variety of situations

Education

- Georgia Institute of Technology, Scheller College of Business, Atlanta GA. Masters of Business Administration, Finance emphasis.

- Georgia Institute of Technology, Scheller College of Business, Atlanta, GA. Bachelors of Science, Management with Accounting emphasis.

Certifications

- Certified Public Accountant (CPA) — State of Georgia

- Accredited in Business Valuation (ABV)

- Accredited Senior Appraiser (ASA)

- Certified Exit Planning Advisor (CEPA)

Read More

GABB Covid-19 Update: Loans, Lending and Liability

The second round of the SBA’s Paycheck Protection Program funding, released Monday April 27, is being distributed by SBA lenders, and is expected to be depleted within just a few days, David Brindley, VP of Small Business Lending at Live Oak Bank, told the GABB in a Zoom meeting on April 28.

David Brindley

Brindley also said the new round of PPP funding is tied to the SBA’s 7(a) loan program, the SBA’s primary program for providing financial assistance to small businesses. The 7(a) program will also be depleted when the PPP runs out of funds, although he anticipated that Congress would approve additional funding in the near future, although “we don’t know when for sure.”

Hear what Brindley had to say at the meeting at this link.

Many other SBA lenders in the GABB told us that they were extremely busy working on PPP loan applications that had been submitted earlier. “For the last month, it has been all hands on deck as everyone in the bank jumped in to help process PPP loans,” Brindley said. Like many other banks, Brindley’s bank “took the approach that we would take care of existing customers first and then open up for new customers.”

His bank temporarily paused most other lending in March to focus on the relief lending through the CARES Act. When the 7A program resumes, Brindley says he expects the SBA to guarantee 90 percent of the loan, as opposed to the 75 percent they have covered in the past. Lenders are going to take a new approach to due diligence, he said. Live Oak looks favorably upon businesses with a strong cash flow and good management.

“We will also require projections from buyers,” Brindley said, to make sure they really understand the cash flow and working capital needs of the business. Also, as part of the CARES Act, the government will make the first 6 months of payments for new SBA loans that close before September 2th.

He ran down a list of potential questions for future SBA loan applicants, including whether the business closed during the quarantine, were customers and suppliers significantly impacted by the shutdown, what disaster funding did the business receive, and why does the buyer think it’s prudent to go forward with a business purchase in the midst of uncertainty.

“We’re going to do even more due diligence than we did before,” Brindley said. “We want to make sure there’s more working capital built into our projects.” Toward that end, his bank — the largest SBA lender in the country — will add additional working capital into loans so that businesses have adequate operating capital in reserve.

“We are open for business right now,” Brindley said. “for historically strong transactions and we are willing to use a common-sense approach to mitigate a Q2 Covid 19-related impact to the business. If we can see that a seller’s revenues are trending back to historic levels and there is sufficient working capital built into the deal structure, we will look at transactions today.”

Larry Domenico

Attorney and GABB Affiliate Lawrence Domenico, a partner in the law firm of Mozley, Finlayson & Loggins LLP, discussed potential liability as businesses prepare to reopen fully or partially. The Georgia Governor has issued specific guidelines for businesses to safely open, as has the CDC.

“I’ve never said ‘it’s not clear, or I don’t know” so many times in my practice of law as in the last couple of weeks.” Language within the gubernatorial order appears to exempt reopened businesses from liability, but it isn’t clear that will give businesses blanket immunity. If a business misses covering one of the safety items listed in the order, maybe you don’t get protection from liability. Traditional body of common law considers whether an entity acted reasonably, and there is varying advice on that front.

“Every business owner is going to have to decide for themselves what is reasonable,” said Domenico. “I think if you try to follow the CDC guidelines, try to follow the governor’s orders, you will have a pretty good defense, but I’m not going to be able to tell you you’re in the clear no matter what.”

The GABB plans to have weekly Zoom meetings on Tuesdays for updates on aid available during the COVID-19 crisis. Check our blog for information on joining future calls.

Read More

An Unexpected Symptom of COVID-19 – Impairment Expense

By David Hern, CPA/ABV, ASA, GABB Affiliate and financial analyst

If you haven’t heard of COVID-19 or Coronavirus–or as my 6-year-old refers to it, the ball with red broccoli on it–then you’ve been living under a rock. Regardless of your quarantine efforts, your business is experiencing a severe coronavirus symptom that could have a major impact on your 2020 financials and audit. For any company that completed an M&A transaction in the last few years, large impairment expenses are likely to occur by this time next year.

COVID-19: my 6-year-old refers to it as the ball with red broccoli on it

Many companies are in the throes of their 2019 audits and are thankful they do not have to pile yet another item on their to-do list. These same companies are probably finishing up purchase price allocations (PPAs) for ASC 805 – Business Combination accounting from deals completed in 2019. However, CFOs and Controllers across the US need to be developing and saving their current COVID-19 financial projections immediately. Why? For starters, many of these companies likely chose to switch to amortizing goodwill over a 10-year period after completing their PPA. What these executives do not realize is just because you are writing off intangible assets does not mean they do not need to be tested for impairment. U.S. generally accepted accounting principles require you to test your goodwill for impairment expense under FASB ASC 350 if there has been a “trigger event.” I can promise you every auditor worth their salt across this great land is going to define a global pandemic which we’ve not seen the likes since the Spanish Flu will as a “trigger event.” At one point, the major stock indices were down well over 30% from their highs.

There are several triggering events noted in ASC Topic 350 that could apply including:

- Macroeconomic conditions such as a deterioration in general economic conditions,

- Overall financial performance such as a negative or declining cash flows or a decline in actual or planned revenue or earnings,

- A sustained decrease in share price, etc.

Consequently, valuation analysts will have to be engaged to determine if a decline in fair values of various reporting units are below their carrying amounts resulting in an impairment expense. Sofer Advisors would be happy to talk with you about your unique circumstances and how they may be a triggering event. Please contact us for a free consultation.